By Terry L. Headley, MBA

President, The Hedley Company: Communications and Research for Energy

Executive Summary

The U.S. natural gas market this week delivered a classic case of extreme weather-driven volatility followed by rapid recalibration, underscoring both the sector’s resilience and its sensitivity to short-term fundamentals.

Winter Storm Fern’s Legacy: The massive Arctic blast in late January triggered the largest weekly storage withdrawal on record—360 Bcf for the week ending January 30, per the EIA—surpassing the five-year average by 89% (170 Bcf). This historic draw stemmed from record demand spikes (seven-day average of 167.4 Bcf/d across residential, commercial, power, and industrial sectors) and temporary production freeze-offs (up to 17 Bcf/d lost at peak). Inventories ended the week at 2,463 Bcf, flipping to a slight 1.1% deficit versus the five-year average but remaining 1.7% above year-ago levels. The event highlighted natural gas’s critical role in powering the grid and heating homes during extremes, while exposing persistent regional constraints, particularly in the Northeast where cash prices soared dramatically.

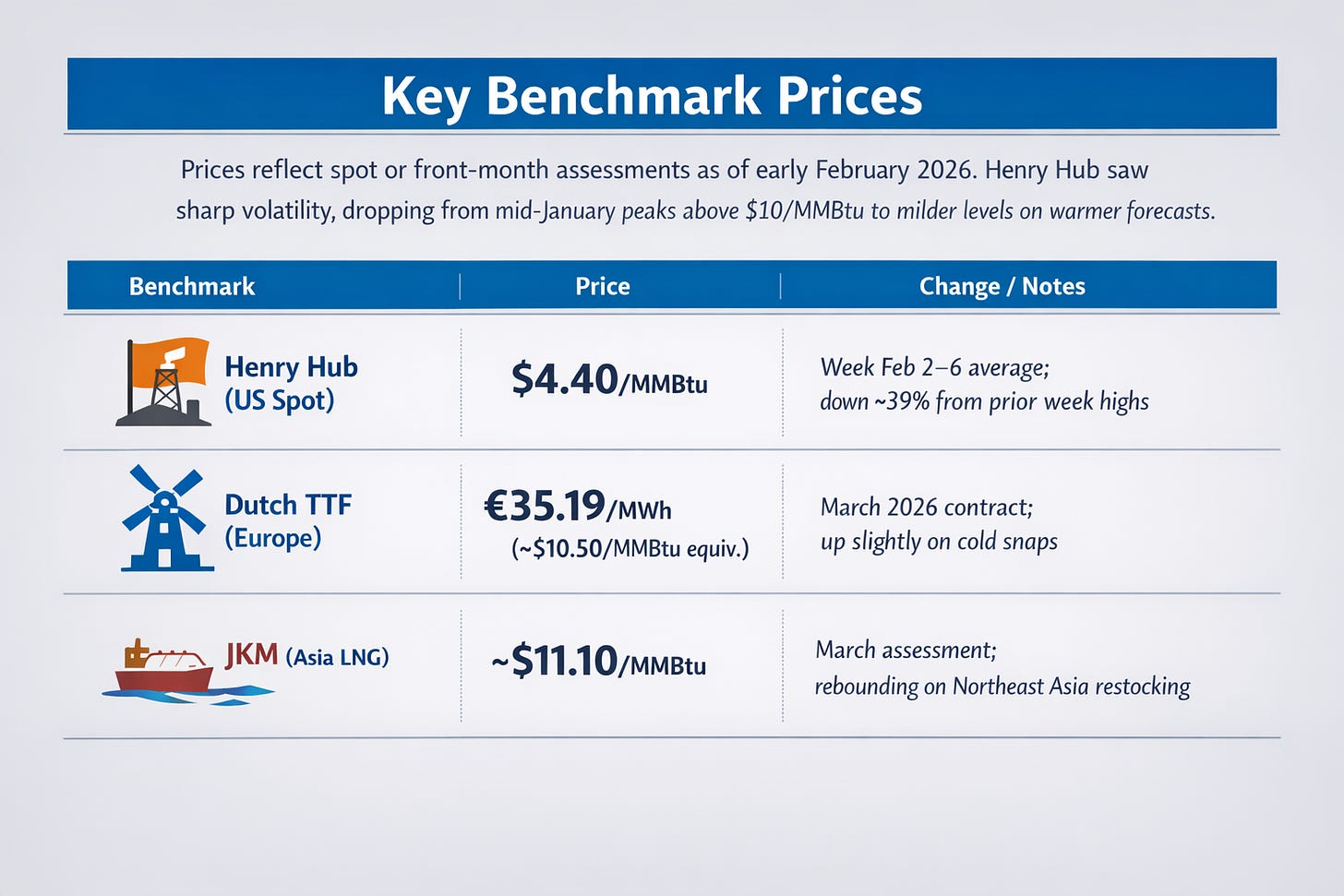

Price Rollercoaster: Henry Hub spot prices hit extraordinary highs during the storm (peaking around $28–$30/MMBtu per various reports) before collapsing sharply on milder February forecasts. The March 2026 futures contract settled around $3.40–$3.50/MMBtu by week’s end, down significantly from intra-storm surges and reflecting trader focus on upcoming warmer weather and ample remaining supplies. This volatility—described as the sharpest single-day drop in nearly 30 years—muted the bullish impact of the record draw, with speculative positioning remaining cautious.

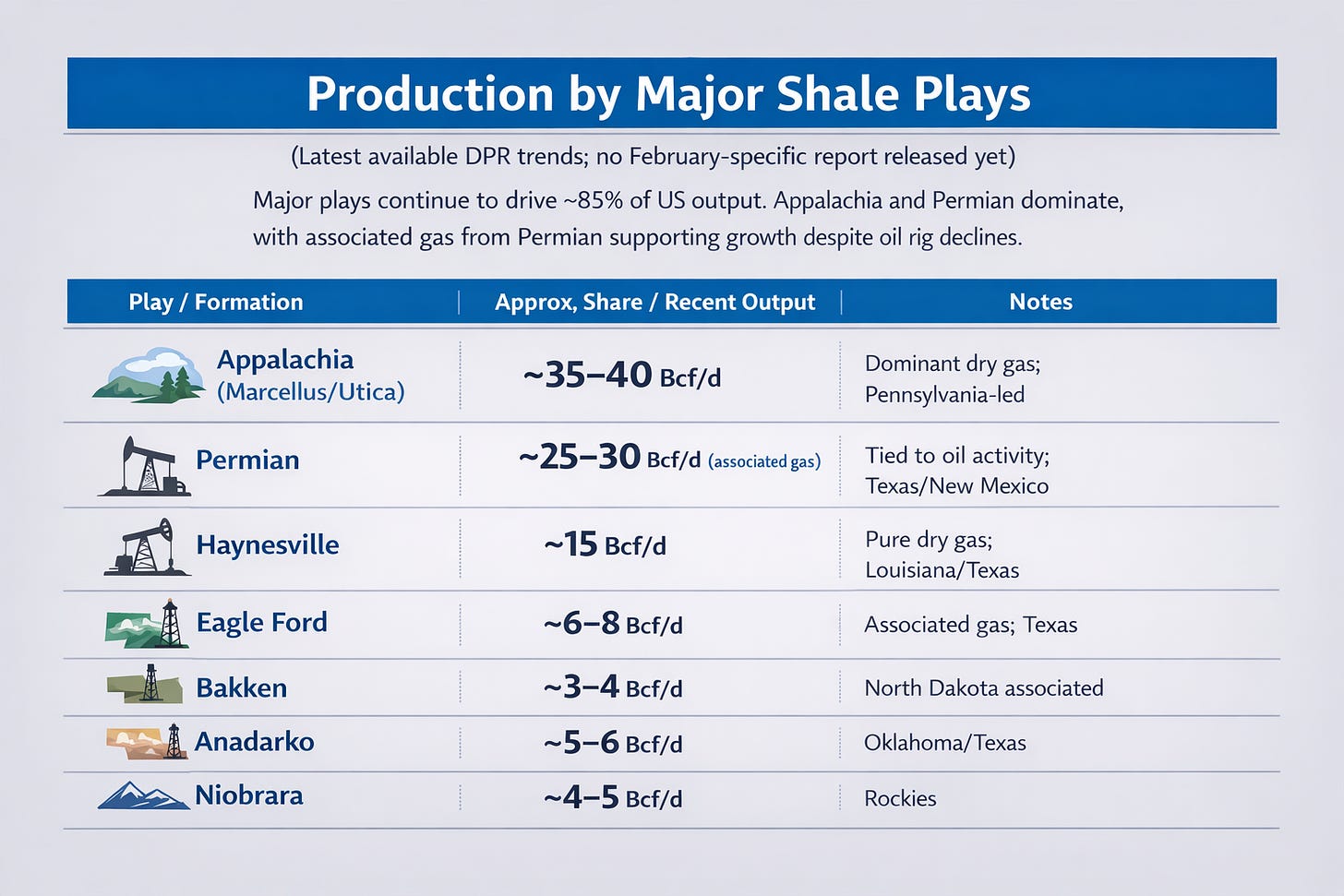

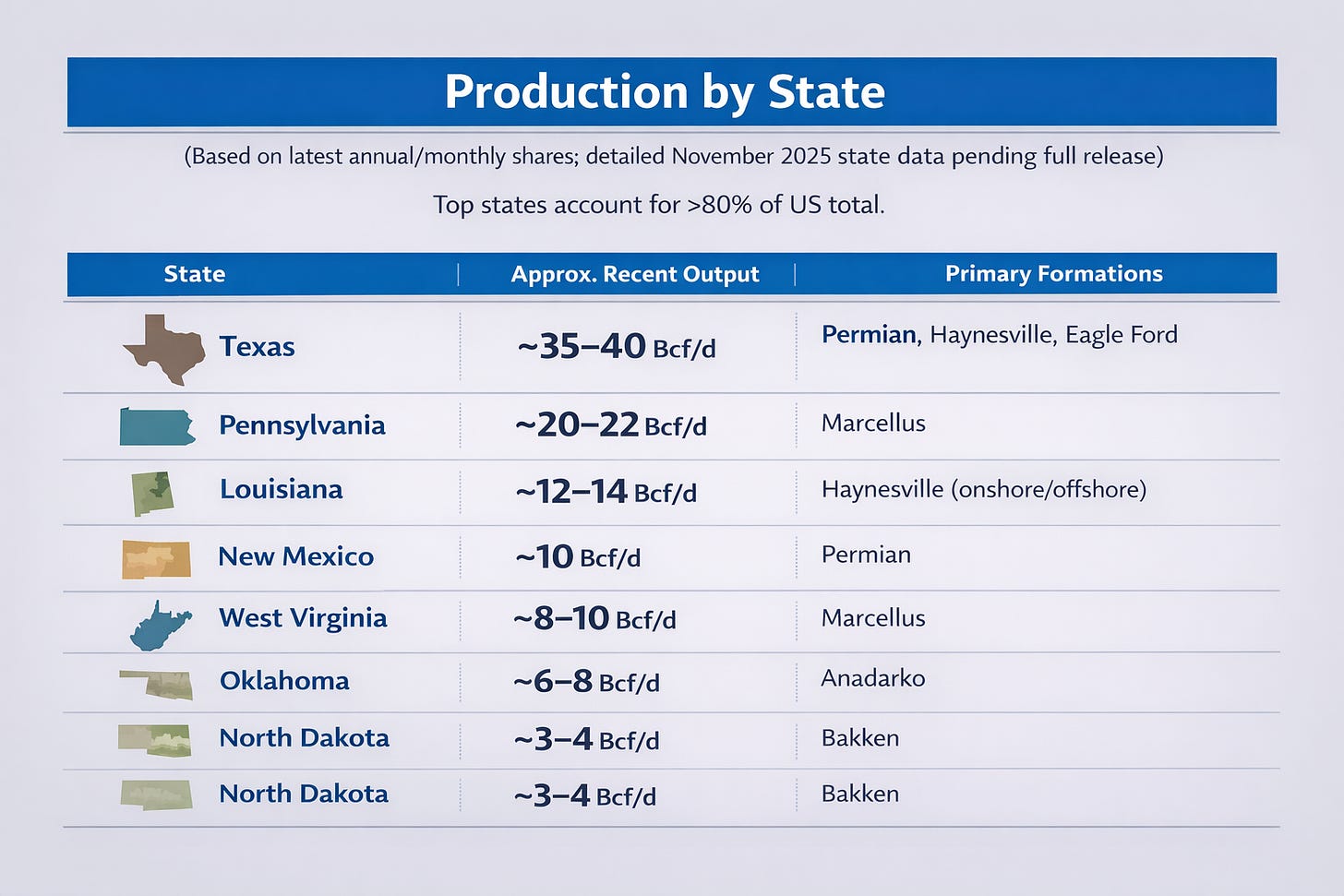

Production and Supply Response: Lower-48 dry gas production dipped to as low as 94 Bcf/d during freeze-offs but rebounded quickly to 105–106 Bcf/d by early February, supported by resilient output in key basins like the Northeast and Rockies. Recent rig counts show gas-directed drilling at a multi-year high (130 rigs), signaling producer readiness to respond to demand signals. EIA forecasts point to modest annual growth, averaging ~109 Bcf/d in 2026, led by Permian associated gas and takeaway capacity additions.

Broader Context and Forward Look: While the storm tested near-term reliability, the bigger story remains structural demand growth from LNG exports (expected 7–10% increase in 2026 volumes as new trains ramp) and rising power burn tied to AI/data centers. These anchors provide a long-term floor, even as global LNG supply additions risk softer international prices and export margins. Regulatory developments, including FERC project approvals and ongoing methane fee implementation, continue to shape infrastructure and compliance landscapes.

In summary, this week’s headlines were dominated by Fern’s dramatic impacts, but the market’s swift return to milder pricing reminds us that weather remains the dominant short-term variable. Beneath the noise, abundant domestic supply, export flexibility, and emerging power-sector demand position the U.S. natural gas industry for sustained relevance—provided midstream expansions keep pace.

US News

Title: US Natural Gas Plunges by Most in About 30 Years on Warm Weather

Publication: Bloomberg

Date: February 2, 2026

Summary:

US natural gas futures experienced their largest single-day percentage decline in nearly 30 years as mid-February weather forecasts shifted to significantly warmer conditions, reducing expected heating demand. The March contract settled sharply lower, reversing recent gains driven by prior cold weather.

Why It Matters:

Extreme price volatility tied to weather shifts underscores the sensitivity of US natural gas markets to short-term demand fluctuations, affecting producer revenues and consumer bills.

Title: Are Physical Natural Gas Buyers Willing to Pay a Higher Henry Hub Basis Price? Winter Storm Fern Provides Clues

Publication: Natural Gas Intelligence (NGI)

Date: February 4, 2026

Summary:

The February 2026 bidweek trading period proved highly volatile due to Winter Storm Fern’s demand surge, forcing physical buyers to confront elevated Henry Hub basis premiums. The event offered insights into how end-users respond to extreme weather-driven price spikes.

Why It Matters:

Buyer tolerance for premium pricing during weather events reveals market depth and resilience, critical for understanding physical delivery dynamics in the US.

Title: Record Natural Gas Stock Withdrawals During Week Ending January 30, 2026

Publication: U.S. Energy Information Administration (EIA)

Date: February 5, 2026

Summary:

Lower 48 working natural gas stocks dropped by a record 360 Bcf amid intense heating demand from Winter Storm Fern, marking the largest weekly withdrawal on record. Inventories fell sharply but remained above the five-year average heading into February.

URL:

https://www.eia.gov/todayinenergy/detail.php?id=67124

Why It Matters:

Record draws signal robust winter demand and potential for tighter supplies later in the season, influencing price expectations and injection needs.

Title: Winter Storm Fern Nearly Pushes 2026 Natural Gas Demand Into Growth Mode

Publication: Natural Gas Intelligence (NGI)

Date: February 5, 2026

Summary:

Lower 48 natural gas demand roared back in early February as Winter Storm Fern drove double-digit percentage increases in power generation and residential/commercial heating burns. The surge nearly flipped year-on-year demand into positive territory after a sluggish January.

Why It Matters:

Weather-driven demand spikes highlight natural gas’s critical role in power and heating, with implications for annual consumption trends and market balance.

Title: Midmorning Markets: All-Time High Storage Pull Fails to Impress Natural Gas Futures Traders

Publication: Natural Gas Intelligence (NGI)

Date: February 5, 2026

Summary:

The EIA’s report of a record 360 Bcf storage withdrawal prompted only a muted futures response, as traders focused on upcoming milder weather and ample remaining inventories. Prices traded in a narrow range despite the historic draw.

Why It Matters:

Bullish fundamental data not moving prices shows how forward weather outlooks currently dominate trader sentiment in the US market.

Title: Natural Gas Market Indicators – February 5, 2026

Publication: American Gas Association (AGA)

Date: February 5, 2026

Summary:

Near-record daily consumption across residential, commercial, power, and industrial sectors drove massive storage withdrawals following Winter Storm Fern. Inventories entered February above the five-year maximum before the historic pull.

URL:

https://www.aga.org/research-policy/resource-library/natural-gas-market-indicators-502nd-edition

Why It Matters:

Comprehensive sector-by-sector data provides a benchmark for tracking consumption patterns and storage health in the domestic industry.

Title: Winter Storm Fern Exposes Northeast Supply Constraints, Sends Natural Gas Prices Soaring

Publication: Natural Gas Intelligence (NGI)

Date: February 6, 2026

Summary:

Winter Storm Fern severely strained Northeast pipeline deliverability, causing regional cash prices to spike dramatically amid competition for limited supply. Infrastructure bottlenecks were laid bare during peak demand.

Why It Matters:

Persistent regional constraints emphasize the need for pipeline expansions to ensure reliable delivery and price stability in high-demand areas.

Title: Williams Weighs Buying Gas-Producing Assets to Enhance AI Energy Supply

Publication: Reuters

Date: February 6, 2026

Summary:

Pipeline giant Williams Companies is exploring acquisitions of natural gas production assets to secure feedstock for rising power demand from data centers and AI operations. This potential move would mark a shift into upstream for the midstream operator.

Why It Matters:

Surging AI-related power needs are prompting vertical integration strategies, signaling long-term structural demand growth for US natural gas.

Title: Hedge Funds Slash Bullish Natural Gas Bets to 13-Month Low

Publication: Bloomberg

Date: February 6, 2026

Summary:

Money managers cut net long positions in US natural gas to the lowest level in over a year following mild weather forecasts and the post-storm price collapse. Speculative sentiment turned cautious despite recent fundamental tightness.

Why It Matters:

Shifts in speculative positioning can amplify price swings and provide insight into broader market expectations for supply and demand.

Title: Natural Gas News - February 6, 2026

Publication: Mansfield Energy

Date: February 6, 2026

Summary:

Futures stabilized above $3.50 after the record 360 Bcf withdrawal, with market attention turning to AI-driven demand resurgence and ongoing weather impacts. The report recapped storm-related records and emerging bullish structural themes.

URL:

https://mansfield.energy/2026/02/06/natural-gas-news-february-6-2026

Why It Matters:

Daily recaps tie short-term events to longer-term trends like technology-fueled demand, helping contextualize weekly developments for industry stakeholders.

International News

Title: European Gas Prices Drop to Lowest Since 2021 on Mild Weather, High Storage

Publication: Bloomberg

Date: February 3, 2026

Summary:

Dutch TTF natural gas futures fell below €30/MWh as unseasonably warm February weather reduced heating demand across Europe. Storage sites remained over 70% full, providing a strong buffer against supply risks.

Why It Matters:

Sustained low prices ease inflation pressures for European households and industry but signal potential oversupply risks heading into the 2026-27 winter.

Title: QatarEnergy Signs 20-Year LNG Supply Deal with India’s Petronet

Publication: Reuters

Date: February 4, 2026

Summary:

QatarEnergy agreed to supply an additional 1.5 million tonnes per year of LNG to Petronet LNG starting in 2028, reinforcing Qatar’s position as a top supplier to South Asia. The deal includes flexible destination clauses to accommodate shifting Asian demand.

Why It Matters:

Long-term contracts lock in supply security for growing Asian economies while supporting Qatar’s massive North Field expansion.

Title: JKM LNG Spot Price Rebounds on Northeast Asia Restocking

Publication: S&P Global Platts

Date: February 5, 2026

Summary:

The Japan-Korea Marker (JKM) for March delivery climbed above $12/MMBtu as Chinese and South Korean buyers stepped up spot purchases ahead of late-winter cold snaps. Tender activity increased markedly after January’s subdued buying.

Why It Matters:

Rising Asian spot demand highlights the region’s pivotal role in setting global LNG prices and absorbing new supply volumes.

Title: Russia’s Gazprom Reports Record Pipeline Gas Exports to China via Power of Siberia

Publication: Interfax

Date: February 5, 2026

Summary:

Gazprom announced that daily flows through the Power of Siberia pipeline reached new highs in January 2026, with annual volumes on track to exceed contractual obligations. The pipeline continues to offset lost European volumes for Russia.

URL:

https://interfax.com/newsroom/top-stories/2026-02-05-gazprom-record-china-exports

Why It Matters:

Growing Russia-China gas trade reshapes Eurasian energy flows and reduces Moscow’s dependence on European markets.

Title: European Underground Gas Storage Ends January at 73% Full

Publication: Gas Infrastructure Europe (GIE)

Date: February 2, 2026

Summary:

EU+UK storage levels stood at 73% (approximately 780 TWh) at the end of January, well above the five-year average despite colder-than-normal weather in parts of northwest Europe. Withdrawal rates slowed as February forecasts turned milder.

URL:

https://www.gie.eu/transparency/storage-inventory

Why It Matters:

Robust storage provides Europe with strong supply security for the remainder of winter and negotiating leverage in upcoming LNG and pipeline contract talks.

Title: Australia’s LNG Exports Hit Record High in January 2026

Publication: EnergyQuest

Date: February 6, 2026

Summary:

Australian LNG exports reached 8.2 million tonnes in January, driven by strong deliveries to China, Japan, and South Korea from projects like Gorgon and Ichthys. Total 2025-26 fiscal year volumes remain on pace for another annual record.

URL:

https://energyquest.com.au/news/australia-lng-exports-january-2026-record

Why It Matters:

Australia’s reliability as the world’s largest LNG exporter underpins Asian energy security amid competing supply from Qatar and the US.

Title: Germany’s Uniper Secures Additional Floating LNG Regas Capacity in Rotterdam

Publication: Argus Media

Date: February 4, 2026

Summary:

Uniper booked extra slots at the Netherlands’ Gate terminal and Eemshaven FSRU to ensure diversified LNG supply through 2028. The move reflects continued caution over Russian pipeline risks despite current oversupply.

URL:

https://www.argusmedia.com/news/2026-02-04-uniper-secures-rotterdam-fsrn-capacity

Why It Matters:

Ongoing investment in import infrastructure signals Europe’s long-term shift toward global LNG markets even as near-term prices soften.

Title: Middle East Tensions Push LNG Freight Rates Higher

Publication: Financial Times

Date: February 6, 2026

Summary:

Red Sea shipping disruptions forced more LNG carriers to reroute around Africa, driving spot charter rates above $100,000/day. Qatar and UAE cargoes to Europe faced the longest delays.

URL:

https://www.ft.com/content/2026-02-06-middle-east-tensions-lng-freight-rates

Why It Matters:

Geopolitical risks remain a key upside driver for global delivered LNG costs despite ample physical supply.

Title: Japan’s LNG Inventories Rise to Multi-Year Highs Ahead of Spring

Publication: Reuters

Date: February 7, 2026

Summary:

Japanese utilities reported LNG stocks at power plants and terminals reached the highest seasonal levels since 2019 as mild weather curbed burn and imports stayed elevated. Companies plan to resell excess spot volumes into the Asian market.

URL:

https://www.reuters.com/business/energy/japan-lng-inventories-multi-year-high-2026-02-07

Why It Matters:

High inventories in the world’s largest LNG importer could cap near-term price upside and increase spot cargo availability.

Title: Global LNG Trade Set for 8% Growth in 2026, Led by Asia and New Supply

Publication: Shell LNG Outlook 2026 (preview release)

Date: February 5, 2026

Summary:

Shell’s annual forecast projected global LNG demand growth of around 8% year-on-year in 2026, driven by Asian economic recovery and power sector switching. Supply additions from Qatar, US, and Australia are expected to keep markets balanced.

URL:

https://www.shell.com/energy-and-innovation/natural-gas/lng-outlook-2026-preview

Why It Matters:

Structural demand growth in Asia reinforces the outlook for sustained global LNG investment despite short-term volatility.

Legislative, Regulatory and Judicial News

Title: DOJ Files Statement of Interest Supporting Stay of Injunction on Enbridge Line 5 Pipeline

Publication: U.S. Department of Justice

Date: February 4, 2026

Summary:

The Justice Department submitted a statement of interest in federal court urging a stay of a district court injunction that would require Enbridge to cease operations on Line 5 through tribal lands in Wisconsin. The filing argues that abrupt shutdown would disrupt energy supply and contradict federal approvals.

Why It Matters:

Ongoing Line 5 litigation poses risks to Great Lakes regional natural gas and crude transport, with potential knock-on effects for Midwest gas deliverability.

Title: FERC Approves Southeast Supply Enhancement Project Expansion

Publication: Federal Energy Regulatory Commission (FERC)

Date: February 3, 2026

Summary:

FERC issued a certificate for Williams’ Southeast Supply Enhancement Project, adding 1.3 Bcf/d of capacity on the Transco pipeline system to serve growing Southeast demand. The approval followed streamlined review procedures introduced in late 2025.

URL:

https://www.ferc.gov/news-events/news/ferc-approves-southeast-supply-enhancement-project-2026

Why It Matters:

New interstate capacity supports rising power generation and LNG export demand in the region, easing potential bottlenecks.

Title: Army Corps Releases Final EIS for Enbridge Line 5 Tunnel Project

Publication: U.S. Army Corps of Engineers

Date: February 6, 2026

Summary:

The Corps published its final environmental impact statement for the proposed Line 5 tunnel under the Straits of Mackinac, advancing the permitting process toward a record of decision expected later in 2026. The report concluded risks could be adequately mitigated.

URL:

https://www.usace.army.mil/Media/News/NewsRelease/Article/2026-02-06/line-5-tunnel-final-eis

Why It Matters:

Progress on the tunnel could secure long-term operation of the pipeline, critical for propane and natural gas liquids supply in the Upper Midwest.

Title: Texas RRC Assesses $1.4 Million in Penalties for Natural Gas Violations

Publication: Railroad Commission of Texas (RRC)

Date: February 5, 2026

Summary:

Commissioners approved enforcement actions totaling over $1.4 million against operators for violations including improper flaring, pipeline safety lapses, and reporting failures in the Permian Basin. Several cases involved excess methane venting.

URL:

https://www.rrc.texas.gov/news/2026-02-05-enforcement-actions

Why It Matters:

Heightened state enforcement reinforces compliance with flaring and emissions rules amid federal methane fee implementation.

Title: FERC Issues Delegated Orders on Multiple Natural Gas Projects

Publication: Federal Energy Regulatory Commission (FERC)

Date: February 3, 2026

Summary:

In its February 3 delegated orders, FERC granted extensions for several pipeline and storage projects and approved minor amendments to existing certificates. Notable actions included commencement deadline extensions for Gulf Coast LNG-related facilities.

URL:

https://www.ferc.gov/news-events/news/delegated-orders-february-3-2026

Why It Matters:

Routine extensions maintain project timelines amid financing and construction challenges in the post-LNG pause era.

Title: EPA Begins Collecting 2026 Methane Waste Emissions Charge Data

Publication: U.S. Environmental Protection Agency (EPA)

Date: February 2, 2026

Summary:

EPA reminded operators that reporting for the 2026 Waste Emissions Charge on excess methane begins with subpart W submissions due March 31, with the $1,500/ton fee applying to emissions above thresholds. Guidance clarified calculation methodologies.

URL:

https://www.epa.gov/inflation-reduction-act/methane-charge-2026-reporting-reminder

Why It Matters:

The escalating fee incentivizes leak detection and repair investments, potentially raising upstream costs but driving long-term emissions reductions.

Title: Ninth Circuit Hears Oral Arguments in California LNG Terminal Challenge

Publication: Reuters

Date: February 5, 2026

Summary:

The U.S. Court of Appeals for the Ninth Circuit heard arguments in a challenge to FERC’s approval of a West Coast LNG export terminal revival, with environmental groups alleging inadequate climate review. No immediate ruling was issued.

URL:

https://www.reuters.com/legal/ninth-circuit-california-lng-challenge-2026-02-05

Why It Matters:

Outcome could influence future FERC consideration of indirect emissions in LNG project approvals.

Title: Pennsylvania DEP Issues Record Permits for Marcellus Wells

Publication: Pennsylvania Department of Environmental Protection

Date: February 4, 2026

Summary:

DEP reported issuing a post-pandemic high of new well permits in January, reflecting accelerated activity tied to AI data center power demand projections. Streamlined reviews contributed to the uptick.

URL:

https://www.dep.pa.gov/Newsroom/2026-02-04-marcellus-permit-record

Why It Matters:

Faster state permitting supports production growth needed for rising associated gas supply in the Appalachian basin.

Title: House Energy Subcommittee Holds Oversight Hearing on FERC Gas Policies

Publication: House Committee on Energy and Commerce

Date: February 6, 2026

Summary:

The Subcommittee questioned FERC commissioners on pipeline certification timelines and affordability impacts, with members pressing for further acceleration of infrastructure approvals. Testimony highlighted AI-driven demand growth.

URL:

https://energycommerce.house.gov/hearings/2026-02-06-ferc-oversight

Why It Matters:

Congressional scrutiny signals potential legislative push for even faster natural gas infrastructure development.

Title: PHMSA Proposes Updates to Gas Pipeline Incident Reporting Requirements

Publication: Pipeline and Hazardous Materials Safety Administration (PHMSA)

Date: February 7, 2026

Summary:

PHMSA issued a notice of proposed rulemaking to expand immediate reporting thresholds for natural gas distribution and transmission incidents, including lower-volume leaks with safety implications. Comments are due in 60 days.

URL:

https://www.phmsa.dot.gov/news/2026-02-07-incident-reporting-nprm

Why It Matters:

Enhanced reporting will improve safety data transparency and support integrity management programs across the aging US pipeline network.

Production and Price

Natural Gas and LNG Market Data Snapshot

US Natural Gas Production

Latest detailed monthly data is preliminary for November 2025 (released early 2026). Daily estimates for early 2026 hover around 107–110 Bcf/d, with temporary dips from Winter Storm Fern freeze-offs followed by quick recovery.

• US Dry Natural Gas Production (Total): 110.1 Bcf/d (November 2025 prelim.; +~2.3% MoM)

• US Gross Withdrawals: ~130.6 Bcf/d (recent monthly estimate)

• 2026 Annual Forecast (EIA): ~107.4 Bcf/d average (down slightly from prior estimates on lower prices)

LNG Highlights

• US LNG Exports: 35 cargoes shipped (week ending February 4, 2026; up 4 from prior week) → Equivalent to ~17–18 Bcf/d feedgas demand at peak.

• Global LNG Market: Supply growth accelerates to >7% in 2026 (IEA), led by US and Qatar. Market “finely balanced” but risks oversupply if Asian demand lags. Key demand centers: Northeast Asia restocking, Europe rebuilding stocks.

This data reflects the latest available from EIA, Platts, and market reports as of February 8, 2026. Let me know if you’d like charts, deeper dives into any category, or to move to the next newsletter section (e.g., storage recap or executive summary)!

Employment and Well Counts

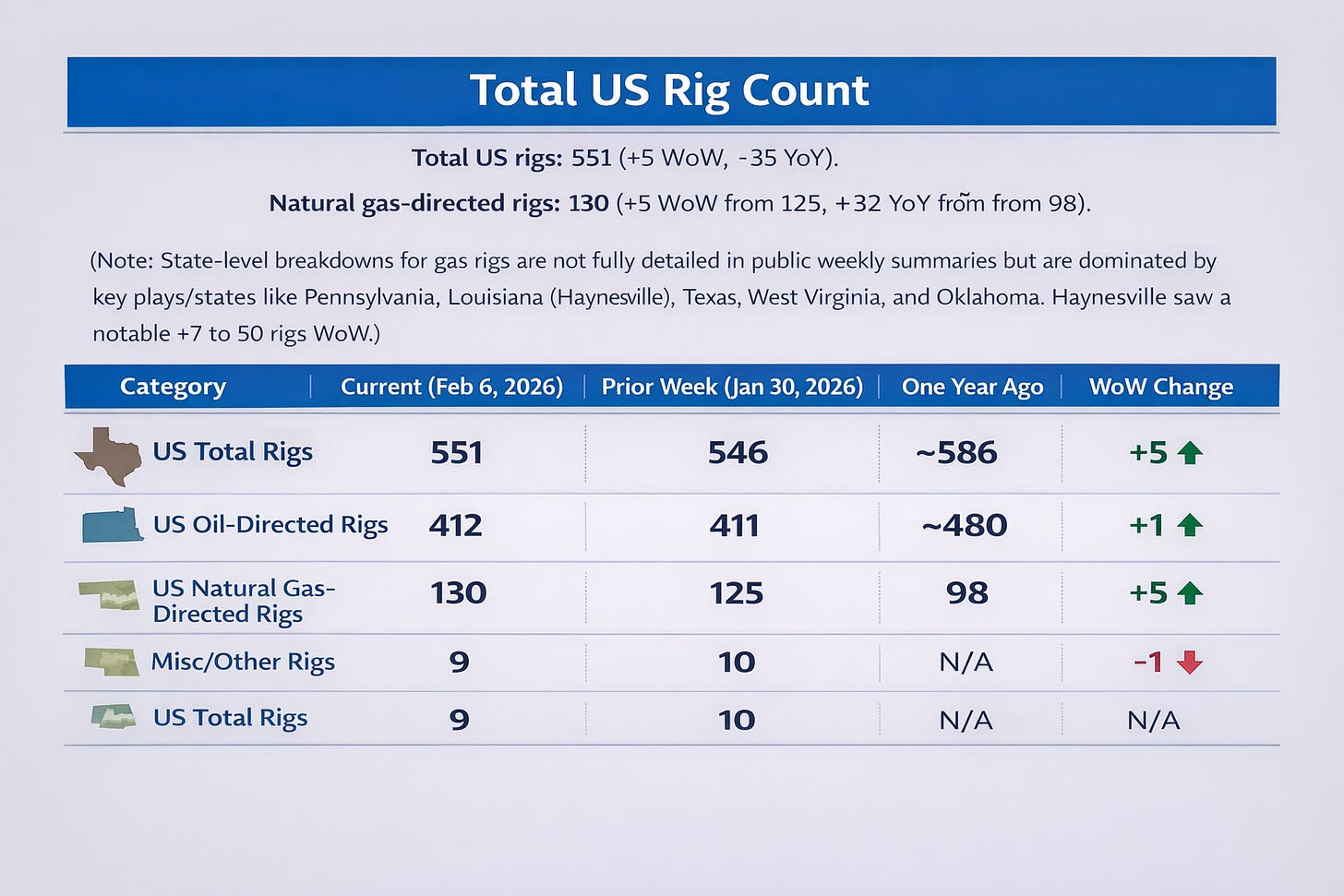

Rig Counts

(Baker Hughes North American Rotary Rig Count, Week Ending February 6, 2026)

Rig counts serve as a leading indicator for new well activity in natural gas-targeted drilling.

• Key States/Plays Insight: Gas rig gains were led by Haynesville (LA/TX) and likely Appalachia (PA/WV). No full state-by-state gas rig split is publicly released weekly, but top gas states align with production leaders (e.g., PA ~20–30% of gas rigs historically).

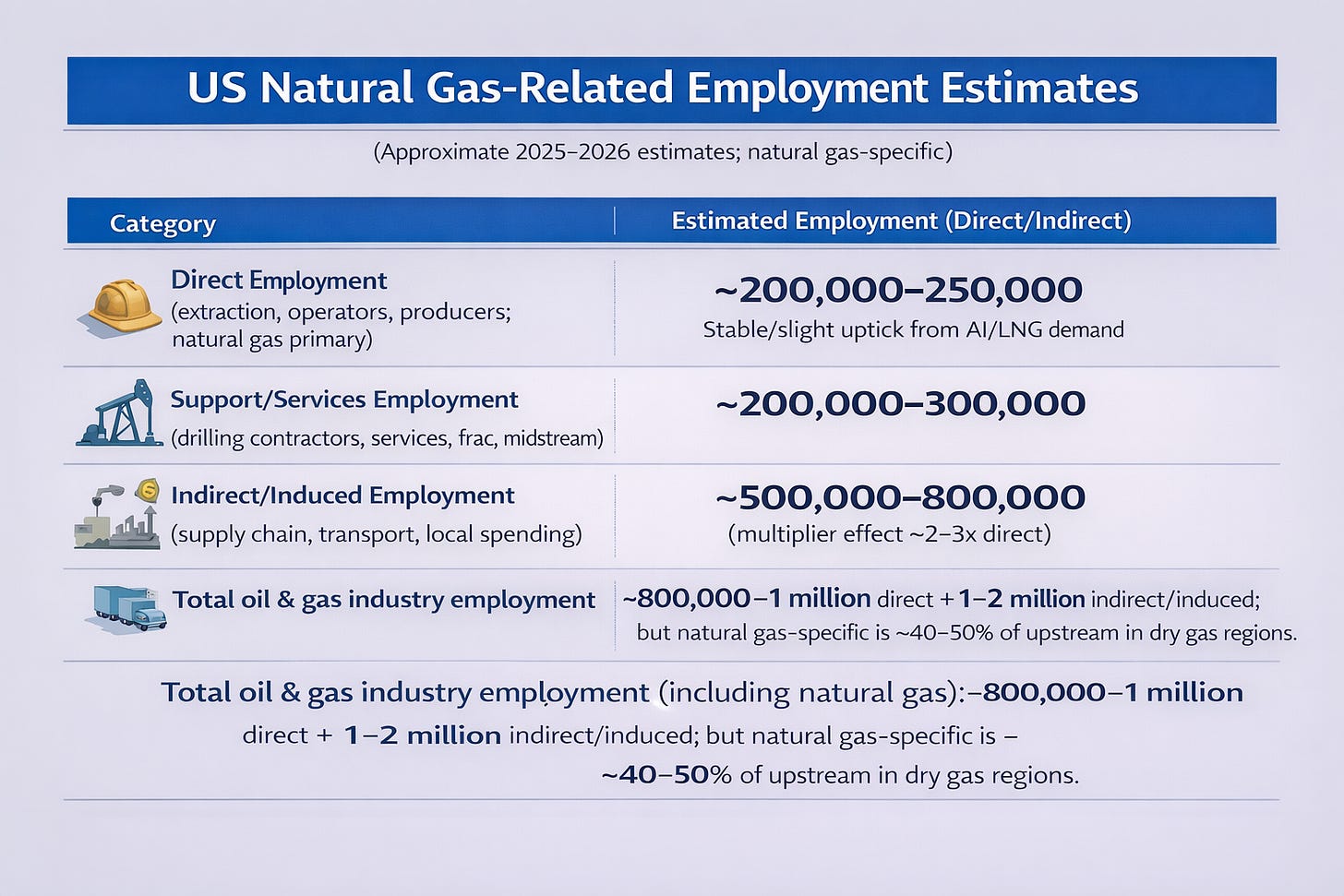

Employment in US Natural Gas Industry

Employment data is typically annual or quarterly (latest comprehensive from 2025 USEER report and BLS trends through late 2025/early 2026). The natural gas sector (extraction, support, midstream) supports ~1–1.5 million direct jobs nationally, with broader oil & gas (including associated gas) at higher levels. Estimates blend natural gas-focused roles (e.g., dry gas plays like Marcellus/Haynesville) with total upstream/support.

Estimated Wages Paid

Average annual wages in natural gas/oil upstream are high due to skilled labor (2025 BLS/USEER data: extraction ~$100,000–120,000 avg.; support ~$90,000–110,000). Estimates use mid-range figures for 2026 (slight inflation adjustment).

• Direct: Avg. $110,000/year → Total est. wages ~$24–33 billion annually.

• Support/Services: Avg. $100,000/year → Total est. ~$22–35 billion.

• Indirect/Induced: Avg. $70,000–90,000/year (broader economy) → Total est. ~$42–90 billion.

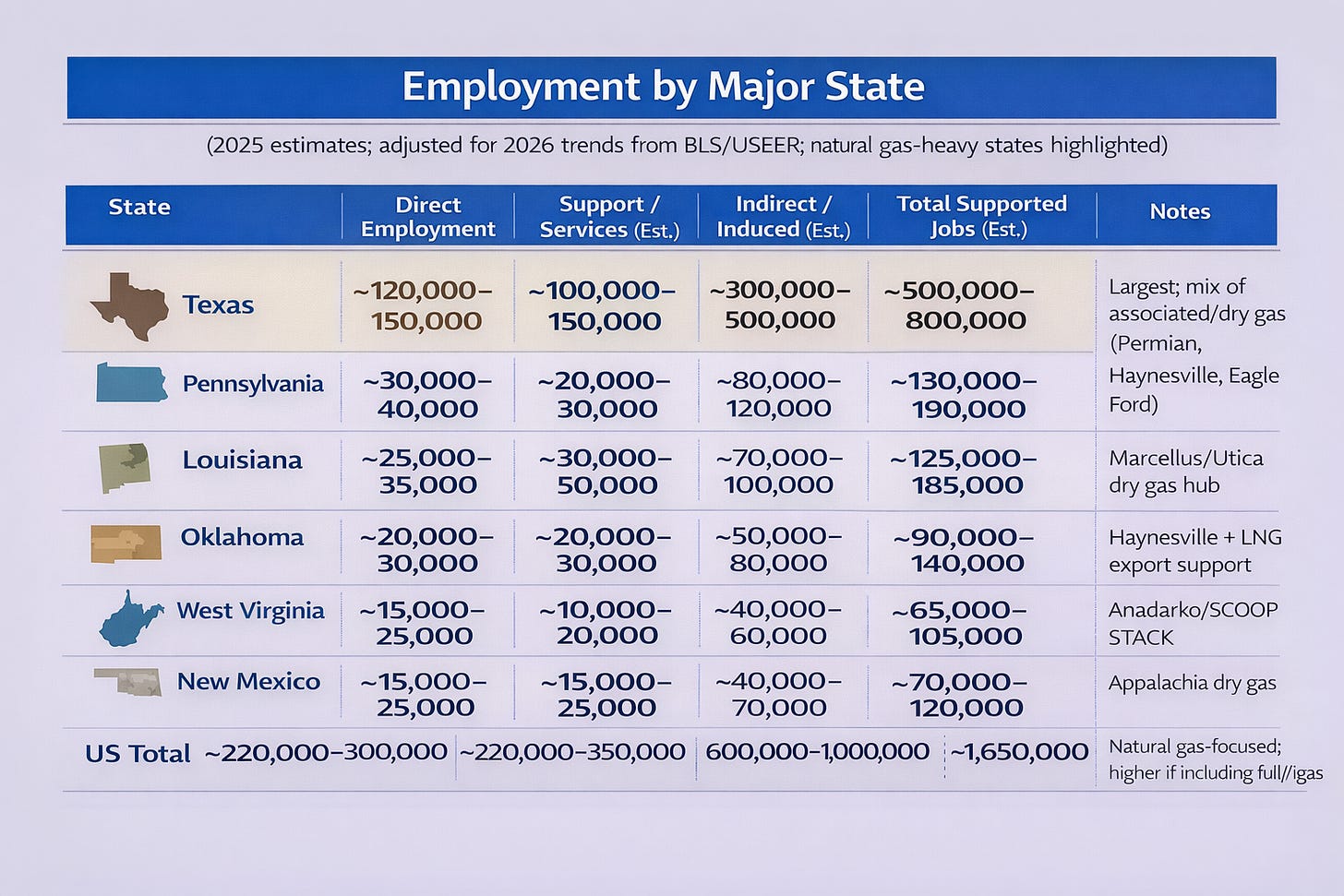

By State Examples (annual est. wages paid, in billions USD; rough based on employment and avg. wages):

• Texas: ~$15–25 billion (direct/support combined).

• Pennsylvania: ~$4–7 billion.

• Louisiana: ~$4–8 billion.

• US Total: ~$50–100+ billion in wages/salaries across categories.

These figures reflect a resilient sector with LNG export and power demand (e.g., AI data centers) supporting activity despite price volatility. Rig gains signal potential future production upside.

SWOT ANALYSIS

Next Week (Mid-February 2026 Outlook)

Strengths

• Record storage withdrawal (360 Bcf in late January) demonstrates strong domestic demand resilience during cold snaps, with production quickly rebounding post-freeze-offs (Lower 48 output nearing 108–110 Bcf/d).

• LNG feedgas demand remains flexible and high (~17–19 Bcf/d), acting as a domestic “relief valve” by redirecting volumes during peaks and supporting export reliability.

• Elevated rig counts in gas-directed plays (130 rigs, up WoW) signal quick supply response capability.

Weaknesses

• Extreme short-term price volatility (sharp post-storm drop on warmer forecasts) exposes producers to revenue swings and basis blowouts in constrained regions (e.g., Northeast).

• Lingering weather sensitivity: Milder mid-February outlooks could accelerate injection season start, pressuring near-term prices downward.

• Regional infrastructure bottlenecks persist, limiting optimal flow during demand spikes.

Opportunities

• Any lingering or unexpected cold snaps could tighten balances further, supporting spot price rebounds and cash market strength.

• Export flexibility: High LNG utilization provides upside if domestic demand softens, redirecting gas abroad.

• Data from recent storm reinforces natural gas’s reliability for heating/power, potentially boosting policy/consumer support.

Threats

• Rapid weather shift to warmer conditions risks oversupply signals, muting bullish storage draw momentum.

• Speculative positioning remains cautious (hedge funds at low net longs), amplifying downside if fundamentals soften.

• Short-term production recovery delays in freeze-affected areas could create brief tightness but more likely lead to oversupply perception.

Next Six Months (Through August 2026 Outlook)

Strengths

• Abundant, low-cost supply base: US production forecast ~107–108 Bcf/d average in 2026, led by Permian/Haynesville/Appalachia associated and dry gas growth.

• Structural demand anchors: LNG exports as largest incremental driver (~9% growth in 2026 volumes from Plaquemines, Corpus Christi Stage 3 ramps, Golden Pass startup mid-year), plus rising power burn from AI/data centers.

• Competitive global position: US LNG remains cost-advantaged and flexible (destination clauses), supporting export growth even in softer international prices (e.g., TTF/JKM softening but demand steady in Asia/Europe).

Weaknesses

• Price outlook muted: Henry Hub expected ~$3.50/MMBtu annual average (flat/slightly down YoY), with summer weakness possible amid ample supply.

• Margin pressures for LNG exporters: Narrowing global spreads (Henry Hub vs. international benchmarks) squeeze offtake economics, though cancellations unlikely in 2026.

• Capital discipline among producers limits aggressive growth, potentially delaying response to demand surges.

Opportunities

• Export surge potential: New capacity additions (e.g., Golden Pass trains, others) drive ~7–10% global LNG supply growth, with US share leading; Asia (China/India restocking) and Europe (diversification from Russia) absorb volumes, tying domestic prices to global upside.

• AI/data center boom: Structural power demand growth favors gas as reliable “bridge” fuel, spurring pipeline expansions and production in key basins.

• Global rebalancing: LNG wave improves affordability, spurring emerging market switching from coal/oil, benefiting US as top exporter.

Threats

• Global oversupply risk: 2026 LNG glut (new capacity from Qatar/US/Australia) pressures international prices downward, narrowing export margins and indirectly capping Henry Hub.

• Regulatory/policy shifts: Potential changes in permitting, methane fees, or export policies could slow infrastructure/LNG ramps.

• Demand uncertainties: Weaker-than-expected Asian growth, European efficiency gains, or delayed coal retirements could soften power burn; geopolitical risks (e.g., shipping disruptions) add volatility.

Overall, the US natural gas industry remains fundamentally strong with export-led demand providing a long-term floor, but near-term faces weather-driven volatility and longer-horizon risks from global supply abundance. Producers benefit from cost advantages and demand diversity (domestic + exports), positioning the sector well for structural growth despite price moderation in 2026.

Op-Ed: LNG Exports and AI Demand Are Reshaping Natural Gas—Not Just Another Winter Storm

The 800-pound gorilla in this week’s natural gas headlines isn’t the record 360 Bcf storage withdrawal from Winter Storm Fern, dramatic as it was. Nor is it the subsequent plunge in Henry Hub prices—the sharpest single-day drop in nearly 30 years—as warmer mid-February forecasts erased storm-driven gains. Those events grabbed the spotlight: a brutal Arctic blast exposed vulnerabilities in production freeze-offs (up to 17 Bcf/d lost at peak), pipeline constraints in the Northeast, and the system’s heroic response, with demand spiking to record seven-day averages of 167.4 Bcf/d. Yet beneath the volatility lies a far larger, structural force reshaping the industry: surging, relentless demand from liquefied natural gas (LNG) exports and AI-powered data centers.

This week’s news cycle—dominated by Fern’s aftermath—perfectly illustrates the disconnect. The storm tested short-term resilience, proving natural gas remains America’s indispensable fuel for heating and power during extremes. Record withdrawals flipped inventories from surplus to slight deficit versus five-year averages, and prices briefly soared before collapsing on mild outlooks. Traders shrugged off the historic draw, focusing instead on forward weather. But this weather-whiplash masks the real story unfolding over months and years.

Look beyond the weekly storage report. LNG exports have quietly become the marginal demand driver, with new capacity ramps (Plaquemines, Corpus Christi Stage 3, upcoming Golden Pass) poised to push U.S. volumes higher in 2026. Forecasts show export growth of 7–10% this year, tying domestic balances to global markets where Asia restocks and Europe diversifies from Russian supplies. Meanwhile, the AI boom accelerates: data centers, hungry for reliable, always-on power, are projected to add billions in electricity demand. Natural gas, as the flexible backbone of the grid, is expected to meet a significant share—potentially requiring 10–15% more U.S. production by the early 2030s just to keep pace with these loads, on top of LNG needs.

The gorilla? It’s this dual, compounding demand wave—LNG + AI/data centers—arriving amid disciplined producer capital spending and lingering infrastructure hurdles. Producers face a familiar dilemma: fundamentals tighten (structural demand anchors, constrained supply growth by choice and pipes rather than geology), yet prices languish in the $3.50–$4.00 range for much of 2026, reflecting oversupply fears from the global LNG wave and weather moderation. Equity valuations struggle, speculative bets stay cautious, and headlines fixate on daily swings rather than the supercycle brewing.

This isn’t hype. Multiple analyses—from Forbes to RBN Energy to the Hamm Institute—highlight how LNG has already transformed balances, while data centers represent a “second pillar” of power burn growth. Pipeline expansions (potentially 200 bcma added in 2026) are racing to catch up, but bottlenecks persist, as Fern reminded us in the Northeast. If demand materializes as projected, the U.S. could see production climb toward 118 Bcf/d or more, with Henry Hub finding a higher floor over time. Yet short-term volatility—tied to weather, global spreads, and regulatory risks—keeps the market pricing caution.

Policymakers and investors should stop chasing storms and recognize the gorilla: America’s abundant, low-cost natural gas is uniquely positioned to fuel both energy security abroad (via exports) and technological dominance at home (via AI). The industry has the supply muscle; the question is whether midstream and policy keep pace to unlock it fully. Ignoring this structural shift risks underinvesting in the very infrastructure that powers the future—while over-relying on volatile weather narratives misses the bigger picture.

In the end, Winter Storm Fern was a loud reminder of natural gas reliability. But the quiet, unstoppable rise of export and digital demand is the force that will define the sector for years. Until the market fully prices that reality, the 800-pound gorilla will keep lurking in the room, even as headlines scream about the latest cold snap or warm spell.

About the Author

Terry L. Headley, MBA, MA, is a veteran energy communicator, strategist, and researcher with more than 25 years of experience at the intersection of energy policy, industrial economics, and public affairs. A former journalist, he has served as a communications director and senior advisor for major energy and coal industry organizations, where he helped shape national and state-level debates over grid reliability, fuel diversity, and energy security.

Headley is widely recognized for developing data-driven messaging strategies that translate complex energy and industrial issues into plain language for policymakers, media, and the public. He is the author of multiple books and long-form studies on energy policy, public relations strategy, and the political economy of America’s industrial base. His work focuses on reliability, affordability, and the often-overlooked role of dispatchable energy in supporting modern society.

About The Hedley Company

The Hedley Company is a strategic communications, research, and advisory firm specializing in energy, industrial policy, and infrastructure issues. The firm provides clients with rigorous analysis, message development, media strategy, and thought leadership focused on grid reliability, fuel diversity, critical minerals, and the economic foundations of American industry.

With deep roots in the energy sector, The Hedley Company works with trade associations, policymakers, industry leaders, and advocacy organizations to ensure complex technical issues are communicated clearly, credibly, and effectively. Its work emphasizes facts over ideology and operational reality over theory, helping decision-makers navigate high-stakes policy environments.

About The Seneca Center for Energy and Critical Minerals Policy

The Seneca Center for Energy and Critical Minerals Policy is a research and policy organization dedicated to advancing serious, fact-based discussion on America’s energy security, electric grid reliability, and critical minerals supply chains. The Center focuses on the strategic importance of traditional and emerging energy resources in supporting national security, economic stability, and industrial competitiveness.

Through original research, policy analysis, and public education, the Seneca Center examines the real-world consequences of energy and environmental policy decisions, with particular attention to dispatchable power, supply chain resilience, and the risks of over-reliance on intermittent resources. Its mission is to bring realism, rigor, and historical perspective back into energy policy debates.

Contact Information

Terry L. Headley, MBA, MA

President, The Hedley Company

📧 Email: [email protected]

📞 Phone: 681-279-0484