A PUBLICATION OF THE HEDLEY COMPANY | WEEK ENDING MARCH 29, 2026 | PUBLISHER T.L HEADLEY

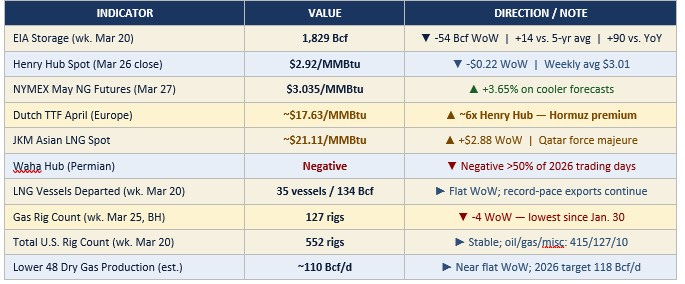

KEY SUMMARY SIGNALS

EXECUTIVE SUMMARY

CHARLESTON, W.Va. — The American natural gas industry enters the week of March 29, 2026, holding the most strategically enviable position in its history — and largely unable to exploit it.

Henry Hub is at $2.92. Dutch TTF is at $17.63. Asian LNG spot (JKM) is at $21.11. That three-way ratio — roughly 1:6:7 — is not a market anomaly. It is a direct measurement of the gap between where U.S. natural gas is produced and where it can physically be exported. The Hormuz disruption that severed Qatar’s LNG supply from global markets has done nothing to tighten the U.S. domestic market because domestic supply — running at approximately 110 Bcf/d — exceeds domestic demand in the shoulder season. All the bullish global pressure exists in the molecules that have already cleared U.S. export terminals; molecules still waiting inland cannot be transported fast enough to close the spread.

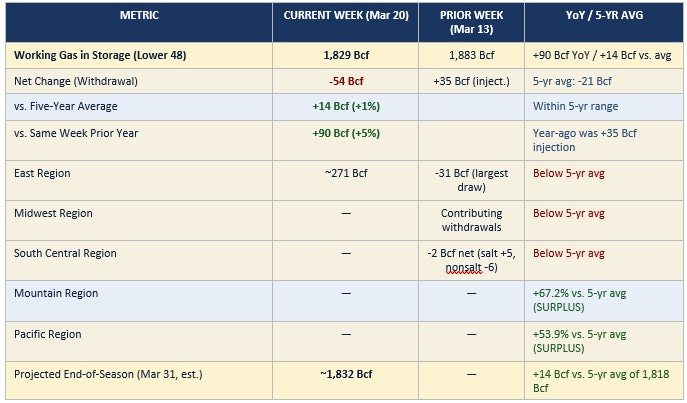

The EIA Weekly Natural Gas Storage Report for the week ending March 20 showed a 54 Bcf net withdrawal — 33 Bcf above the five-year average for the period — leaving working gas in storage at 1,829 Bcf. Inventories are 14 Bcf (1%) above the five-year average and 90 Bcf (5%) above the same week last year. The withdrawal season is effectively over; market attention is already pivoting to the spring injection cycle, where the question is how quickly utilities will rebuild storage heading into next winter.

On the global side: QatarEnergy remains under force majeure on Ras Laffan LNG output, EU storage sits at 28.3% capacity with the Netherlands at 6%, and Chevron’s Wheatstone LNG facility in Australia is offline with a return timeline measured in weeks. Three simultaneous supply disruptions hitting the same global market have created an LNG deficit that cannot be resolved by rerouting cargoes that do not exist. The U.S. is the world’s most capable swing supplier — but capacity additions needed to move substantially more gas are not a 2026 event. Golden Pass Train 1 and the remaining Corpus Christi Stage 3 trains are the near-term incremental additions; meaningful new capacity waits until 2027 and beyond.

The EIA March 2026 STEO set the 2026 Henry Hub annual average forecast at $3.80/MMBtu — 13% below the February STEO — and explicitly assumed U.S. gas prices would be ‘relatively unaffected’ by the Hormuz disruption. That assumption is being tested. Henry Hub May futures closed Friday at $3.035, and Barclays is maintaining its base case that Hormuz reopens by early April. If it does, much of the global LNG premium deflates rapidly. If it does not, the pressure on export capacity infrastructure intensifies.

Sources: EIA Weekly Natural Gas Storage Report (released March 27, 2026, week ended March 20); EIA March 2026 STEO (March 10, 2026); Baker Hughes Rig Count (week ended March 25); EIA/Bloomberg LNG vessel data; GIE AGSI (March 27, 2026).

SECTION 1 — NATURAL GAS STORAGE

Source: EIA Weekly Natural Gas Storage Report (Form EIA-912), released March 27, 2026, for week ending March 20, 2026.

The 54 Bcf withdrawal for the week ended March 20 was the second-largest for that calendar week in the last five years, driven by lingering late-winter heating demand in the East and Midwest. The 33 Bcf bullish deviation versus the five-year average was primarily weather-driven — colder-than-normal temperatures in the mid-Atlantic and Northeast contributed approximately 27 Bcf of the differential, with supply/demand fundamentals accounting for roughly 6 Bcf of the remaining tightness. Despite the headline withdrawal, the East, Midwest, and South Central regions remain at storage deficits versus five-year norms, while the Mountain and Pacific regions carry significant surpluses — a structural West-to-East pipeline flow dynamic that favors basis strength at Eastern hubs heading into summer. The market is transitioning to injection season; the first injection of 2026 was +35 Bcf the prior week (March 13). Expect modest injections through April as heating demand fades and production maintains near-record pace.

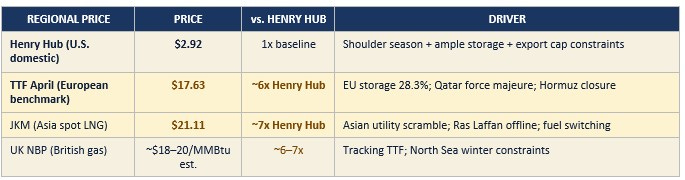

SECTION 2 — NATURAL GAS PRICES: DOMESTIC & INTERNATIONAL

Sources: Henry Hub spot via EIA/FRED (March 26 close); NYMEX May futures via CME/Barchart (March 27 settlement); TTF and JKM via EIA Weekly Natural Gas Storage Report Supplement (week ending March 20) and Bloomberg Finance.

The 1:6:7 Spread — What It Means:

Henry Hub at $2.92 versus TTF at $17.63 versus JKM at $21.11 is the defining fact of the current U.S. natural gas market. The spread is not a trading opportunity the market has missed. It is a physical constraint: the U.S. does not have enough LNG export capacity to arbitrage Henry Hub to parity with global prices. Cheniere’s CFO has stated explicitly that no significant additional output is possible until later in 2026. Every cargo that clears an American LNG terminal effectively earns the exporting entity the TTF or JKM price while paying the Henry Hub input cost — a liquefaction margin that is the most attractive in the history of the U.S. LNG industry. The bottleneck is throughput, and the answer is Golden Pass Train 1, Corpus Christi Stage 3 remaining trains, and the 2027 wave of new capacity. Until then, Henry Hub stays structurally disconnected from global prices — except to the extent that cooler-than-expected spring weather or production disruptions create domestic tightness.

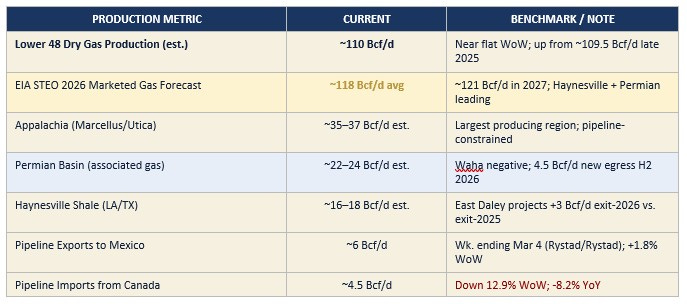

SECTION 3 — U.S. NATURAL GAS PRODUCTION & SUPPLY

Sources: EIA Weekly Natural Gas Storage Report Supplement (week ended March 20, 2026); Wood Mackenzie/Rystad Energy/Bloomberg production data (via AGA Natural Gas Market Indicators, March 5, 2026); EIA March 2026 STEO (March 10, 2026).

U.S. dry gas production is maintaining near the 110 Bcf/d level — a zone that balances robust Permian associated gas output with more measured Haynesville and Appalachian activity in the current price environment. The Permian Basin structural constraint remains the most consequential near-term production story: Waha spot prices have been negative on more than 50% of trading days in 2026, reflecting the inability to move Permian gas eastward fast enough. The four-pipeline solution — Blackcomb (2.5 Bcf/d), Hugh Brinson Phase 1 (1.5 Bcf/d), Gulf Coast Express expansion (570 MMcf/d), and Trident — is scheduled to deliver 4.5 Bcf/d of new Permian egress capacity in the second half of 2026. When that capacity comes online, the Waha discount should collapse and Permian production growth will accelerate sharply. The Haynesville is carrying the LNG export growth story in the meantime. East Daley projects Haynesville production exiting 2026 roughly 3 Bcf/d above where it entered — that is the incremental supply that fills Golden Pass Train 1 and completes the Corpus Christi Stage 3 ramp.

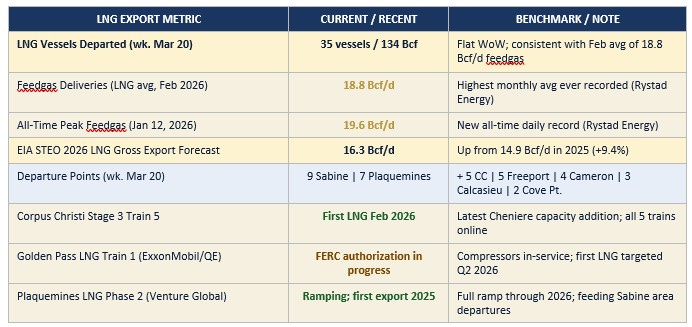

SECTION 4 — U.S. LNG EXPORTS

Sources: EIA Weekly Natural Gas Storage Report Supplement (week ended March 20, 2026); Bloomberg Finance, L.P. (LNG vessel tracking); EIA March 2026 STEO; AGA Natural Gas Market Indicators (March 5, 2026).

Full ramp through 2026; feeding Sabine area departures

The Hormuz disruption has done nothing to expand U.S. LNG export capacity — but it has made every cargo that does depart extraordinarily profitable. U.S. LNG terminals are operating at or near rated capacity. Cheniere’s management explicitly stated that no significant incremental output is possible until later in 2026. The binding constraint is physical: the trains that exist are full, and Golden Pass Train 1 is the next material addition. With QatarEnergy still under force majeure on Ras Laffan and EU storage at 28.3%, the cargo value of each LNG shipment leaving Sabine Pass, Corpus Christi, or Plaquemines today is approximately six to seven times the value at the domestic hub. The strategic case for accelerating the remaining U.S. LNG permit and construction backlog — currently representing 30+ Bcf/d of projects sanctioned in 2025 alone — has never been more concrete.

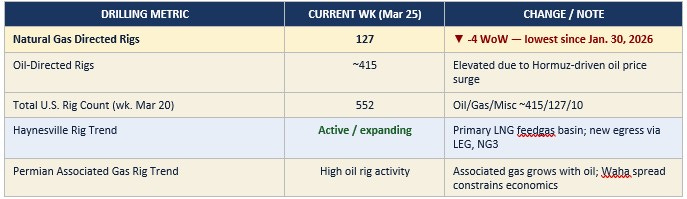

SECTION 5 — DRILLING ACTIVITY & INFRASTRUCTURE

Sources: Baker Hughes Rig Count (week ended March 25, 2026, released March 28); YCharts/AOGR (rig count history); RBN Energy (pipeline infrastructure); AGA Natural Gas Market Indicators (March 5, 2026).

Key 2026 Pipeline Additions — Permian Gas Egress:

• Blackcomb Pipeline (2.5 Bcf/d): H2 2026 targeted; moves Permian gas eastward to Henry Hub area and Gulf LNG.

• Hugh Brinson Pipeline Phase 1 (1.5 Bcf/d): H2 2026 targeted; Port Arthur area delivery — directly feeds Golden Pass LNG.

• Gulf Coast Express Expansion (570 MMcf/d): 2026; additional Permian takeaway toward Gulf markets.

• LEG (Louisiana Energy Gateway, 1.8 Bcf/d): Operational since July 2025; Haynesville to Gillis Hub, supporting LNG feedgas.

• NG3 (New Generation Gas Gathering, 1.7 Bcf/d): Operational since August 2025; parallel Haynesville route to Gulf.

The rig count drop to 127 gas-directed rigs — down 4 from the prior week and the lowest since late January — reflects rational producer discipline in the face of $2.92 Henry Hub pricing. The Permian is not restraining activity on gas rigs because oil rigs are running full-tilt at $90+ Brent; associated gas grows regardless of dedicated gas rig activity. The strategic message for 2026: gas supply growth is largely predetermined by oil-directed Permian drilling and the Haynesville’s proximity to LNG infrastructure. The gas rig count is not the binding variable. Infrastructure throughput is.

SECTION 6 — GLOBAL LNG MARKET & GEOPOLITICS

Sources: EIA Weekly Natural Gas Storage Report Supplement (March 27, 2026); Kpler LNG Market Update (March 10, 2026); GIE AGSI (March 27); CNBC/Bloomberg Hormuz reporting (March 28, 2026); Bloomberg TTF/JKM pricing.

Active Global Disruptions — Week Ending March 29:

• QatarEnergy Force Majeure (Ras Laffan LNG): Iranian missile strikes on Ras Laffan damaged production trains. QatarEnergy declared force majeure on long-term LNG contracts covering buyers in Italy, Belgium, South Korea, and China. Qatar’s 17% share of world LNG capacity is effectively offline with a multi-year repair timeline on the affected trains. This is the largest single LNG supply disruption in history.

• Strait of Hormuz Closure: Effectively closed to most tanker traffic since February 28. Approximately 20–25% of global seaborne oil and ~20% of global LNG transits this waterway. U.S. and allies have released 400 million barrels from strategic oil reserves — the largest release on record. Barclays maintains a base case of Hormuz reopening by early April; oil executives warn the window is closing. If Hormuz stays shut past mid-April, supply disruptions worsen materially.

• Chevron Wheatstone LNG (Australia): Offline with an undisclosed mechanical issue; Chevron warned it could take weeks to ramp back to full capacity. Wheatstone is a 8.9 mtpa facility. The outage adds to global LNG supply tightness at the worst possible moment — peak EU/Asia winter exit demand.

• EU Storage at 28.3% (Netherlands: 6%): GIE/AGSI data as of March 27 shows EU aggregate storage at 28.3% — approximately 20 percentage points below year-ago levels. The European Commission has issued emergency guidance urging immediate refilling efforts. With TTF at $17.63, European buyers are the most aggressive LNG bidders in the global market. Summer 2026 injection targets of 80%+ by November will require historic injection rates.

• Asian LNG Demand Surge: JKM at $21.11/MMBtu, up $2.88 week-over-week. Thailand ordering full coal capacity online in response to LNG price spikes. South Korea and Taiwan switching fuels. Bangladesh boosting coal consumption. Asian LNG analysts targeting $30+/MMBtu in summer and $40+ if Hormuz remains closed six months.

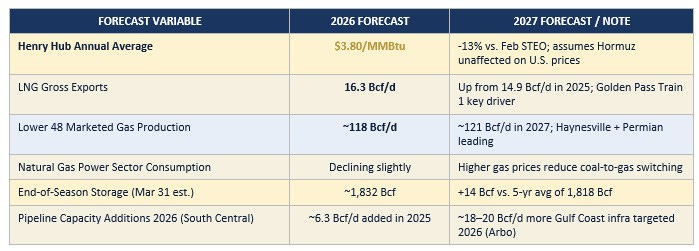

SECTION 7 — EIA MARCH STEO: NATURAL GAS FORECASTS

Source: EIA Short-Term Energy Outlook, March 10, 2026 (next release April 7, 2026). All figures from the March 2026 STEO.

SECTION 8 — NATURAL GAS INDUSTRY NEWS

1. HORMUZ CLOSURE TIGHTENING GLOBAL LNG THROUGH SPRING — U.S. POSITIONED AS SWING SUPPLIER BUT CAPACITY CONSTRAINED

The effective closure of the Strait of Hormuz since February 28 has fundamentally restructured global LNG markets. Qatar’s Ras Laffan facility — supplying roughly 20% of global LNG — remains offline under force majeure. Barclays is maintaining a base case of Hormuz reopening by early April, but oil industry executives are warning that the window is closing and that the economic and market fallout could escalate sharply if reopening does not occur by mid-April. U.S. LNG terminals are running at capacity. Cheniere’s CFO has stated no material additional output is possible until later in 2026. The U.S. is the world’s preferred swing LNG supplier — it simply cannot swing fast enough given current terminal constraints.

Sources: CNBC, March 28, 2026 | URL: https://www.cnbc.com/2026/03/28/oil-gas-prices-iran-war-hormuz.html Bloomberg, March 20, 2026 | URL: https://www.bloomberg.com/news/articles/2026-03-20/how-iran-s-qatar-lng-attack-hormuz-closure-are-driving-up-oil-and-gas-prices

2. EU ISSUES EMERGENCY GAS STORAGE GUIDANCE — 28.3% CAPACITY HEADING INTO INJECTION SEASON

The European Commission issued emergency guidance this week urging member governments to act quickly to begin filling underground gas storage caverns ahead of next winter. EU aggregate storage stood at 28.3% capacity as of March 27 — approximately 20 percentage points below year-ago levels — with the Netherlands at an alarming 6%. Summer 2026 injection targets of 80%+ by November require unprecedented injection rates beginning in April. With TTF at $17.63/MMBtu, European utilities are bidding against Asian buyers for every available Atlantic LNG cargo and are reviving coal purchasing for baseload power. The scale of the European gas deficit is the primary driver of the TTF–Henry Hub spread and will sustain global LNG demand well into 2027 regardless of Hormuz resolution.

Sources: GIE/AGSI, status March 27, 2026 | URL: https://agsi.gie.eu/ Bruegel European Gas Imports dataset, updated March 26, 2026 | URL: https://www.bruegel.org/dataset/european-natural-gas-imports

3. GOLDEN PASS LNG TRAIN 1: FERC AUTHORIZATION PROGRESSING — Q2 2026 FIRST LNG IN SIGHT

Golden Pass LNG (backed by QatarEnergy and ExxonMobil) continues progressing through FERC authorization steps for Train 1 commissioning at its Port Arthur, Texas, facility. Compressor systems and related pipeline infrastructure were placed in service in late 2025. The facility is seeking FERC authorization to run feedgas through the Train 1 turbine for testing. First LNG cargo production is targeted for Q2 2026. At full capacity, Train 1 alone will add approximately 800 MMcf/d in LNG feedgas demand. Trains 2 and 3 are not expected to come online until 2027. With QatarEnergy’s Ras Laffan capacity offline, the strategic and commercial urgency to bring Golden Pass Train 1 online has never been higher — and the irony of the Qatar-backed project ramping up at exactly the moment Qatar’s own export capacity is destroyed is not lost on the market.

Sources: NGI (December 2025); AGA Natural Gas Market Indicators (March 5, 2026) | URL: https://naturalgasintel.com/news/train-1-commissioning-accelerates-at-golden-pass-setting-up-early-2026-lng-production/ AGA: https://www.aga.org/research-policy/resource-library/natural-gas-market-indicators-march-5-2026/

4. WAHA HUB REMAINS NEGATIVE — PERMIAN INFRASTRUCTURE RELIEF DELAYED UNTIL H2 2026

The Permian Basin’s Waha Hub has now recorded negative spot natural gas prices on more than 50% of trading days in 2026. Flaring events are at five-year highs. The structural cause is simple: Permian gas production is outpacing the takeaway capacity of existing pipelines. The solution — the Blackcomb (2.5 Bcf/d), Hugh Brinson Phase 1 (1.5 Bcf/d), Gulf Coast Express expansion (570 MMcf/d), and Trident pipelines — is scheduled for the second half of 2026, but not before then. For the first half of 2026, Permian producers accept negative wellhead prices on associated gas as the cost of running oil operations at elevated oil prices. Once the new pipes come online, Waha should approach parity with the Henry Hub, Permian production will grow rapidly, and additional feedgas volumes will flow to Gulf LNG terminals — with direct connection to Golden Pass LNG via Hugh Brinson.

Sources: RBN Energy (February 20, 2026); NGI (March 2026) | URL: https://rbnenergy.com/daily-posts/blog/pipeline-buildout-set-unlock-permian-natural-gas-production-growth-later-2026

5. HAYNESVILLE PRODUCTION RAMPING — THE CRITICAL FEEDGAS BRIDGE

The Haynesville Shale in northwest Louisiana and northeast Texas remains the most critical near-term supply region for U.S. LNG export growth. With Williams’ Louisiana Energy Gateway (1.8 Bcf/d) and Momentum’s NG3 pipeline (1.7 Bcf/d) both operational, Haynesville gas now has direct, high-capacity routes to Gulf LNG terminals. East Daley Analytics projects Haynesville production exiting 2026 approximately 3 Bcf/d above where it entered the year. Additional storage capacity development in the East Texas/Southwest Louisiana corridor — with open seasons active from multiple operators — reflects growing confidence in sustained LNG demand growth for the region. The Haynesville’s structural advantage: it is a dry gas basin, close to export infrastructure, with ample spare drilling inventory and low breakeven economics at prices above $3.00/MMBtu.

Sources: RBN Energy (January 27, 2026); NGI (January 5, 2026); AGA March 5, 2026 | URL: https://rbnenergy.com/daily-posts/blog/new-pipelines-push-more-haynesville-natural-gas-south-meet-lng-demand

STRATEGIC OUTLOOK

The Price Is Lying

By T.L. Headley, MBA, / President / The Hedley Company

CHARLESTON, W.Va. — Henry Hub at $2.92 per MMBtu is the most misleading number in the energy markets right now. It tells you what American natural gas costs to buy at the Louisiana delivery point. It does not tell you what it costs to deliver that molecule to Tokyo ($21/MMBtu), Bruges ($17.63/MMBtu), or Seoul (also around $21/MMBtu). Those prices represent the true global value of American natural gas. The domestic price is a function of what the infrastructure can move — not what the resource is worth.

The gap between $2.92 and $17.63 is not an arbitrage opportunity the market has missed. Traders know exactly what TTF is. Cheniere knows exactly what TTF is. The gap exists because the physical equipment needed to liquefy and load additional molecules does not yet exist. The trains that are running are full. The EIA’s LNG export forecast for 2026 — 16.3 Bcf/d — reflects what can physically be loaded, not what could theoretically be sold. Every Bcf/d of new export capacity that comes online in 2026 and 2027 will sell into a European and Asian market that is structurally undersupplied for the next several years. The window is not closing. It is opening further.

Domestically, the natural gas market is comfortable bordering on oversupplied. Storage exits winter with a small surplus to the five-year average. Production is holding near 110 Bcf/d. The Permian continues to produce associated gas regardless of the Henry Hub price because the economics are driven by oil at $90+/barrel Brent, not $2.92 natural gas. The shoulder season will bring further price softness as heating demand disappears and production runs flat. The EIA STEO’s $3.80/MMBtu 2026 average forecast assumes Hormuz does not structurally pull U.S. molecules into global markets. That assumption deserves scrutiny — if Hormuz stays closed through April and beyond, the structural pull intensifies and Henry Hub will need to carry a larger risk premium to incentivize producers and infrastructure operators.

The Waha discount is the domestic market telling you something plainly: the Permian has more gas than it can move. That problem resolves itself in the second half of 2026 when 4.5 Bcf/d of new Permian egress capacity enters service. When it does, Waha normalizes, Permian production accelerates, and a new wave of Permian-sourced feedgas hits the Gulf Coast pipeline system — arriving precisely as Golden Pass Train 1 ramps to full capacity and needs molecules. The pieces are all moving toward each other; the timing question is whether the infrastructure comes online before, during, or after the peak of the global LNG shortage.

The gas rig count falling to 127 — its lowest since late January — is rational producer behavior. At $2.92 Henry Hub, the marginal dry gas well in the Haynesville pencils out, but barely. Producers are running the minimum necessary to supply the contracted LNG feedgas volumes and serve growing power demand in the Southeast. They are not drilling for storage. That discipline is appropriate and will sharpen the eventual price response when LNG demand growth and new export capacity cause the domestic supply/demand balance to tighten in 2027.

The Qatar LNG catastrophe has done something important to the long-term narrative: it has demonstrated, beyond any reasonable policy debate, that the world needs more U.S. LNG export capacity — not less. The European Commission is not issuing emergency gas storage guidance because it has too many LNG suppliers. Japan and South Korea are not paying $21/MMBtu because global supply is abundant. The political and economic case for expediting U.S. LNG project permitting and construction — already strengthened by the Trump administration’s energy dominance posture — has been validated by events that no policymaker could have scripted.

Henry Hub at $2.92 is not the price of American natural gas. It is the price of American natural gas that cannot get to the boat fast enough.

— T.L. Headley, MBA

President, The Hedley Company | Founder & VP Communications, The Seneca Center for Energy and Critical Mineral Research

Charleston, W.Va.

GAS CURRENTS — STANDARD DISCLAIMER AND PUBLICATION INFORMATION

Gas Currents is published by The Hedley Company, 169 Raceview Drive, Ona, WV 25545. Publisher: T.L. Headley, MBA, MA. Work phone: 681.279.0484. Work email: [email protected]. All data and analysis are for informational purposes only and do not constitute investment, legal, or regulatory advice.

2026 | A Publication of The Hedley Company | © 2026 T.L. Headley, MBA, MA