A Publication of The Hedley Company • Issue 2 • April 27, 2026

EDITOR’S OPENING BRIEF

The Defense Production Act and the Architecture of Energy Security

CHARLESTON, W.Va. — The Trump administration did something last week that no administration has done in the modern regulatory era: it invoked the Defense Production Act simultaneously across the full U.S. energy supply chain. Five presidential determinations, signed April 20-22 and published in the Federal Register on April 23, classify coal mining and baseload generation, petroleum production and refining, natural gas transmission and LNG capacity, electric grid infrastructure, and large-scale energy development as industrial resources essential to national defense. Taken together, they are the most comprehensive deployment of wartime industrial production authority over the civilian energy sector since the Second World War.

This is not a set of regulatory waivers. This is not a temporary emergency stay of a retirement date. The Defense Production Act Section 303 framework places these energy supply chains in the same statutory category as military aircraft components and strategic petroleum reserves. The Section 303(a)(7) waiver in each determination bypasses standard federal procurement constraints. The Secretary of Energy is now authorized to make direct purchases, contract commitments, and financial instruments to expand capacity in each category — without competitive bidding requirements, without necessity certifications, without the normal procurement timeline. The $1 billion appropriated in the 2025 tax and energy law is the designated funding vehicle, with no guardrails and a spending window through September 30, 2027.

The DPA framework does not ask whether the market will build the infrastructure the grid needs. It directs the federal government to build it. That is a different question — and a different answer.

The timing is not coincidental. The North American Electric Reliability Corporation’s January 2026 Long-Term Reliability Assessment documented that summer peak demand could surge 224 gigawatts over the next decade — 69 percent higher than what NERC projected just one year earlier. Five RTO regions face high reliability risk by 2029. PJM failed to fully clear its reliability requirement at the most recent capacity auction for the first time in its history. The Strait of Hormuz has been largely closed since February 28, removing approximately 20 percent of global LNG supply from seaborne markets and demonstrating in real time what energy infrastructure dependence on geopolitically fragile supply chains produces.

Energy Research Review exists to track the research, technology development, policy architecture, and funding mechanisms that determine whether the United States emerges from its current energy stress with a stronger, more reliable foundation. The DPA determinations are the most significant policy architecture event this publication will cover in its inaugural year. But policy architecture without implementing guidance is intent without execution. Watch the Federal Register. Watch the DOE solicitation calendar. Watch for the implementing rules that will define which projects qualify for Section 303 financing — and whether the $1 billion reaches the infrastructure that actually needs it before the spending window closes in September 2027.

This issue covers the full week ending April 26: the DPA package in detail, the first U.S. primary terbium oxide production at Energy Fuels’ White Mesa Mill (a milestone two decades in the making), the USA Rare Earth Serra Verde acquisition and its implications for the November 2026 China controls deadline, the summer 2026 grid adequacy picture as data center load additions reach historic levels in ERCOT and PJM, and five research and funding items worth the attention of anyone working in the energy technology development pipeline.

The standing promise of this publication: we follow the money through to deployment outcomes, not just press release day.

By T.L. Headley, MBA | President, The Hedley Company

RESEARCH SPOTLIGHT

First U.S. Primary Terbium Oxide in Decades: What Energy Fuels’ White Mesa Milestone Actually Means

NETL’s Appalachian REE pipeline and the technology gap between pilot achievement and commercial scale

On March 25, 2026, Energy Fuels Inc. announced that its White Mesa Mill in Utah had produced the first kilogram of terbium (Tb) oxide from a primary U.S. mineral feedstock. The purity: 99.9 percent, meeting global permanent magnet manufacturer specifications. The feedstock: monazite ore from mines in Florida and Georgia. This achievement, followed by qualification of the company’s dysprosium oxide by a major South Korean automotive manufacturer, marks the first time in many decades that a U.S. facility has demonstrated mine-to-oxide HREE capability at pilot scale from a domestic ore source.

The industrial significance of this announcement requires context that most coverage failed to provide. Terbium is one of the seven heavy rare earth elements placed under China’s active export controls as of April 4, 2025. It is a critical additive in neodymium-iron-boron permanent magnets — the magnets that power EV motors, drone actuators, missile guidance systems, and wind turbine generators. The additive function of terbium is specific: it improves magnetic performance at elevated temperatures, enabling smaller, lighter motors to function reliably in high-heat environments. There is no commercially viable substitute at current technology maturity. And there is, outside China and the Energy Fuels pilot circuit, zero commercial-scale terbium oxide production on Earth.

The Technical Achievement

Energy Fuels’ White Mesa process chain begins with monazite concentrate — a phosphate mineral that occurs as a co-product of heavy mineral sands mining in Florida and Georgia. Monazite has a naturally high rare earth content, typically 50-70 percent rare earth oxides by weight, with a profile that includes both light rare earths (La, Ce, Pr, Nd) and a meaningful fraction of heavy rare earths (Dy, Tb, Sm). The company has been processing monazite for NdPr oxide at commercial scale (approximately 850-1,000 tonnes per year designed capacity) since 2025. The terbium pilot extends that capability into the HREE fraction.

The critical technical step is separation: extracting specific HREE fractions from the mixed rare earth stream at sufficient purity for downstream magnet manufacturing. Energy Fuels achieved 99.9 percent Tb purity using solvent extraction chemistry, exceeding the 99.5 percent automotive specification. The production rate at pilot scale is approximately one kilogram per week. Commercial HREE circuits at White Mesa, which would target up to 48 metric tonnes of dysprosium per year and 14 metric tonnes of terbium per year, are planned to come online in Q4 2026 — contingent on infrastructure investment and sufficient feedstock supply.

The Technology Gap: Pilot to Commercial

The distance from 1 kilogram per week to 14 tonnes per year is not a chemistry problem. The chemistry is proven. The 14-tonne annual target represents approximately 270 kilograms per week — a scale-up factor of 270x from the current pilot rate. That scale-up requires capital investment in solvent extraction circuits, materials handling infrastructure, waste management systems, and quality control validation across production volumes that pilot-scale runs cannot test. It requires a feedstock supply chain capable of delivering monazite at commercial volumes on a consistent schedule. And it requires the magnet manufacturers and OEMs who have requested samples for qualification to complete their validation processes and execute offtake agreements that justify the capital.

Energy Fuels is simultaneously developing international monazite feedstock sources to supplement U.S. mine supply: its Donald Project in Australia and the Vara Mada deposit in Madagascar represent the medium-term feedstock pipeline. The company’s stated timeline for commercial HREE circuit operation — Q4 2026 — lands within the November 10, 2026 expiration date of China’s suspended October 2025 export controls. That overlap is not a coincidence; it is the forcing function that every Western HREE developer is racing toward.

NETL’s Appalachian HREE Pipeline

Parallel to Energy Fuels’ monazite-based pathway, NETL’s CORE-CM (Carbon Ore, Rare Earth, and Critical Minerals) initiative is funding Appalachian coal-stream REE extraction projects aimed at a different feedstock profile: coal seam underclays, acid mine drainage precipitate, and coal fly ash. The CORE-CM program’s stated production target is 1 to 3 tonnes per day of high-purity mixed rare earth oxides from domestic demonstration-scale facilities. Multiple Phase II projects are active in West Virginia, Kentucky, Pennsylvania, and Virginia.

The Appalachian HREE profile differs from monazite in important ways. AMD precipitate from Northern Appalachian treatment sites shows approximately 50 percent critical REE ratio — heavily weighted toward the elements with the most acute supply chain stress. Coal seam underclay REE concentrations run 0.1 to 0.3 percent TREO with a heavy REE component that makes the feedstock strategically attractive even at relatively low bulk concentrations. The University of Texas Bureau of Economic Geology resource assessment estimated that American coal ash deposits alone contain between $8.4 billion and $165 billion in recoverable rare earth elements — with Appalachian coal ash at roughly 585 milligrams per kilogram REE content running significantly richer than Powder River Basin ash at approximately 330 milligrams per kilogram.

The bottleneck NETL identified in its January 2026 research — and which the Energy Fuels pilot confirms in commercial terms — is not resource availability. It is midstream processing capacity. NETL’s ClaiMM digital platform, launched January 23, 2026, was specifically designed to accelerate the data sharing and investment coordination between resource characterization and commercial processing infrastructure. A domestic REE extraction program without parallel midstream separation investment produces feedstock for Chinese processors, not domestic magnets.

Source: Energy Fuels terbium oxide announcement — https://www.prnewswire.com/news-releases/energy-fuels-announces-first-us-primary-production-of-critical-heavy-rare-earth-material-in-decades-302724441.html

Source: NETL CORE-CM Program — https://netl.doe.gov/coal/rare-earth-elements

Source: UT Bureau of Economic Geology REE assessment, IJCST 2026 — https://doi.org/10.1007/s40789-026-00872-y

POLICY & REGULATORY WATCH

The DPA Energy Package: What Five Presidential Determinations Actually Authorize

1. Presidential Determination No. 2026-08: Coal Supply Chains and Baseload Generation Capacity

White House / Federal Register (FR Doc. 2026-08010, 91 FR 21927) | Signed April 20, published April 23, 2026

The coal determination classifies coal mining, rail and barge logistics, export and domestic terminals, generating unit availability and life-extension work, on-site stockpiles, and associated reliability updates as industrial resources, materials, or critical technology items essential to the national defense. The Section 303(a)(7) waiver bypasses all standard procurement requirements. DOE is authorized and directed to implement the determination, including making necessary purchases, commitments, and financial instruments to enable projects. The $1 billion in the 2025 tax and energy law — allocated specifically to ‘carry out the Defense Production Act’ — is designated as the funding vehicle. Availability: through September 30, 2027. Congressional guardrails: none.

WHY IT MATTERS: The coal determination is the statutory instrument that converts emergency plant preservation orders into a capital program. DOE emergency orders under FPA 202(c) mandate that specific plants keep operating — but they provide no mechanism for funding the maintenance, life-extension work, and stockpile investment that operational continuity requires. The DPA Section 303(a)(7) waiver fills that gap with federal procurement authority. DOE implementing guidance has not yet been published; that is the next critical milestone. Watch the Federal Register for a solicitation framework.

Source: White House DPA Coal Determination — https://www.whitehouse.gov/presidential-actions/2026/04/presidential-determination-pursuant-to-section-303-of-the-defense-production-act-of-1950-as-amended-on-coal-supply-chains-and-baseload-power-generation-capacity/

Source: Federal Register FR Doc. 2026-08010 (April 23, 2026) — https://www.federalregister.gov/documents/2026/04/23/2026-08010/presidential-determination-pursuant-to-section-303-of-the-defense-production-act-of-1950-as-amended

2. Companion DPA Determinations: Natural Gas Transmission/LNG, Electric Grid Infrastructure, Petroleum, and Large-Scale Energy Development

White House / The Hill | April 20-22, 2026

Four companion determinations were signed alongside the coal memo. The natural gas transmission and LNG determination covers interstate pipeline infrastructure, compressor stations, LNG export capacity, and LNG storage. The electric grid infrastructure determination covers high-voltage transformers, circuit breakers, substations, and transmission line components — specifically addressing the 12-24 month lead time vulnerability for large power transformers, the majority of which are manufactured outside the United States. The petroleum determination covers domestic crude production, refining, and logistics. All five determinations invoke the same 303(a)(7) waiver and draw from the same $1 billion fund.

WHY IT MATTERS: The transformer supply chain gap has been flagged by NERC, FERC, DOE, and DHS as the most acute physical vulnerability of the U.S. electric grid. A coordinated attack on or failure of 9 to 50 key high-voltage transformer nodes could cause cascading outages affecting tens of millions of customers for months. The DPA grid infrastructure determination creates the first federal mechanism to directly purchase transformers, fund domestic manufacturing capacity, and build strategic reserves — at scale, without standard procurement constraints.

Source: The Hill: Trump Invokes DPA for Energy Infrastructure — https://thehill.com/policy/energy-environment/5840983-trump-defense-production-act-oil-coal-energy-infrastructure/

3. FY2027 Budget: $3.5B Reprogrammed from Hydrogen Hubs to ‘Baseload Power’ Program; NETL Centers of Excellence Structure Formalized

American Public Power Association / NETL / DOE | April 2026

The president’s FY2027 budget request proposes a new ‘Baseload Power’ program within DOE, funded by reprogramming $3.5 billion from the Infrastructure Investment and Jobs Act funding previously designated for regional clean hydrogen hubs. The program would support purchase, construction, and acquisition of plant and capital equipment to increase grid capacity, upgrade infrastructure, and conduct reliability-strengthening activities. The FY2027 budget simultaneously formalizes four NETL Centers of Excellence: coal at Morgantown, WV; oil and natural gas at Pittsburgh, PA; critical minerals and advanced alloys at Albany, OR; and a geothermal center to be designated. Research operations face an 8 percent funding reduction to approximately $80 million under the request; infrastructure funding rises 2 percent to $58 million.

WHY IT MATTERS: The $3.5 billion reprogramming from hydrogen hubs to baseload power is a direct policy statement about the administration’s reliability priorities — and a significant legal and political fight in the making. Hydrogen hub recipients in seven states have contractual expectations that will not be relinquished without litigation. Congressional appropriators, particularly those with hydrogen hub projects in their districts, will resist the reprogramming. ERR will track both the appropriations battle and any legal challenges to the reprogramming authority through the FY2027 budget cycle.

Source: American Public Power Association FY2027 budget analysis — https://www.publicpower.org/periodical/article/president-proposes-cutting-energy-programs-2027-budget

Source: NETL Centers of Excellence / Hoodline — https://hoodline.com/2026/04/pittsburgh-morgantown-crowned-new-hubs-for-fossil-fuel-research

4. EIA Electric Power Monthly (February 2026 Data): Retail Electricity Prices +9.0% YoY; Coal Generation -11.3%

U.S. Energy Information Administration | Released April 23, 2026

EIA’s Electric Power Monthly for February 2026 data (released April 23) reports the national average retail electricity price rose to 14.36 cents per kilowatt-hour — up 9.0 percent year-over-year. All four customer sectors posted price increases: Transportation (+23.6%), Commercial (+10.7%), Industrial (+8.6%), and Residential (+7.4%). Coal consumption for power generation fell 11.3 percent compared to February 2025. Nuclear generation increased 2.1 percent. The report documents that the Northeast saw an 8.2 percent year-over-year increase in total electricity generation — the only region to post an increase — driven by below-normal temperatures that increased residential heating demand.

WHY IT MATTERS: The simultaneous occurrence of a 9.0 percent retail price increase and an 11.3 percent coal generation decline in the same month is the statistical foundation for the reliability-affordability argument: removing dispatchable generation does not reduce electricity prices, it increases them. The 9 percent retail price increase is being felt by every household and business in the country and will show up in utility rate cases, political debates, and energy assistance program requests through the remainder of 2026.

Source: EIA Electric Power Monthly Update (February 2026 data) — https://www.eia.gov/electricity/monthly/update/print-version.php

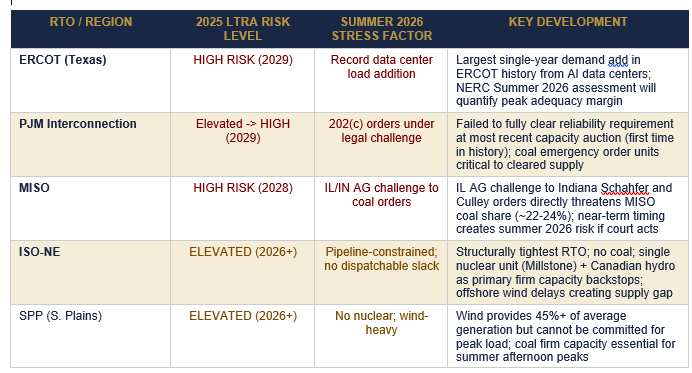

GRID STRESS REPORT

Summer 2026 Adequacy: The Data Center Load Addition That Changes the Math

The North American Electric Reliability Corporation’s Summer 2026 Reliability Assessment, expected in May 2026, will provide the authoritative regional reliability picture heading into peak season. Based on NERC’s 2025 Long-Term Reliability Assessment, the current operating environment, and RTO-level data, the following regions carry the highest near-term adequacy risk for Summer 2026.

Source: NERC Long-Term Reliability Assessment 2025 (January 29, 2026). Summer 2026 stress factors are editor analysis based on current operating conditions and RTO public reporting. NERC Summer 2026 Reliability Assessment expected May 2026.

The Data Center Load Arithmetic

ERCOT’s situation deserves specific quantification. The EIA Annual Energy Outlook 2026 (released April 8) documents that after 15 years of essentially flat U.S. electricity consumption, demand has grown 2.1 percent per year on average over the past five years. ERCOT projects summer peak total internal demand growing from 94,650 megawatts in 2026 to 154,077 megawatts by 2035 — driven in significant part by 23 gigawatts of data center interconnection requests by 2030. That is a 62 percent increase in ERCOT’s peak demand obligation in nine years, in a region with no coal emergency orders, no nuclear additions in the near-term pipeline, and a capacity mix that is approximately 48 percent natural gas and 28 percent wind.

The Spring 2026 demand picture is misleadingly calm. Henry Hub at $2.52 per MMBtu is the lowest since October 2024. Storage injections are running 8 percent above seasonal norms. Wholesale electricity prices across every RTO are at spring trough levels in the $25-50 per MWh range. None of those numbers reflect what the same system looks like at 105 degrees Fahrenheit in Dallas in August with ERCOT’s data center load running around the clock. The spring shoulder season is when summer adequacy decisions need to be made — and the decisions being made now, through emergency order preservation, DPA financing authorization, and capacity auction frameworks, will determine whether the summer grid stress is manageable or an emergency.

WHY IT MATTERS: The summer 2026 adequacy picture is not yet a crisis. It is a high-stakes planning period in which the decisions made now — emergency order preservation, DPA financing deployment, capacity auction clearing — will determine whether summer 2026 is also manageable. The NERC Summer Assessment in May will be the first authoritative public document to quantify the specific regional margins. ERR will cover it in detail.

Source: NERC Long-Term Reliability Assessment 2025 (January 29, 2026) — https://www.nerc.com/globalassets/ourwork/assessments/nerc_ltra_2025.pdf

Source: EIA Annual Energy Outlook 2026 (April 8, 2026) — https://www.eia.gov/outlooks/aeo/

CRITICAL MINERALS & SUPPLY CHAIN

The November 10 Clock: USA Rare Earth’s Serra Verde Acquisition and the Race Against China’s Control Architecture

On April 22, 2026, USA Rare Earth Inc. announced the acquisition of Brazil’s Serra Verde Group in a $2.8 billion cash-and-stock transaction. The headline number is large. The strategic significance is larger. Serra Verde’s Pela Ema ionic clay rare earths mine in Goias State, Brazil is projected to produce 6,400 metric tonnes of total rare earth oxides annually at phase-one capacity — including more than half of all heavy rare earth elements produced outside China. The deposit profile is ionic clay, the same geological formation type that produces over 90 percent of China’s heavy rare earth supply from its southern provinces. The transaction was backed by a U.S. International Development Finance Corporation financing package of $565 million committed to Serra Verde in February 2026, and comes with a 15-year offtake agreement backed by a U.S. government special purpose vehicle.

This is the most consequential Western HREE investment since the original MP Materials-DOD agreement. It is also a transaction with an explicit deadline: November 10, 2026, when China’s suspension of the October 2025 broader export controls expires. That suspension — part of the U.S.-China trade agreement reached following the Xi-Trump meeting — covers the additional five elements placed under control in October 2025, the equipment and technology controls, and critically, the extraterritorial provision that would extend Chinese jurisdiction to overseas products manufactured using Chinese REE materials or technology. Clark Hill PLC’s legal guidance is unambiguous: the suspension is ‘temporary relief but should not be mistaken for deregulation.’

The October 2025 architecture — if reinstated without Western commercial HREE production in place — would affect every NATO-allied manufacturer that uses Chinese REE inputs, regardless of where the final product is assembled. That is not a supply chain vulnerability. That is a supply chain weapon.

The industrial timeline against November 10: MP Materials is targeting mid-2026 commissioning of its HREE separation facility at Fort Worth — within the window. Energy Fuels is targeting Q4-2026 commercial HREE circuits at White Mesa — within the window, narrowly. Serra Verde at USA Rare Earth is producing at phase-one scale now. Northern Minerals’ Browns Range dysprosium-terbium project in Western Australia is advancing toward a final investment decision with current prices providing stronger economic justification than at any prior point. France’s Carester is targeting late-2026 commissioning of a European separation facility.

The Appalachian domestic opportunity sits in parallel with these international supply chain developments, not in competition with them. DOE’s CORE-CM NOFO for commercial-scale Appalachian REE development — expected in 2026 — will be the most important federal funding opportunity for regional REE extraction since the program was established. The Seneca Center for Energy and Critical Mineral Research has completed an inventory of more than 80 former surface mine sites in West Virginia with REE extraction and co-location potential. That inventory is the site-selection database for NOFO applications, and the co-located plasma gasification / REE recovery / data center infrastructure model developed by Heritage Critical Minerals and Eureka Energy is the integrated development architecture that federal program offices should be funding.

The strategic case for acting before November 10 is straightforward: every week of continued suspension is a week of normal supply flow that can be converted into commercial scale-up for Western producers. Every week that passes without additional Western HREE separation capacity narrows the window for a manageable transition if China reinstates the full October architecture. The November deadline is not a negotiating artifact. It is a policy lever Beijing has explicitly said it intends to retain.

WHY IT MATTERS: The Serra Verde acquisition gives USA Rare Earth access to the only known Western HREE deposit profile that is geologically comparable to China’s southern ionic clay production. Combined with Energy Fuels’ terbium pilot, MP Materials’ HREE facility timeline, and the Australian and European capacity additions, the Western supply chain has more concurrent HREE development activity than at any previous point since Chinese consolidation. The question is not whether the supply chain can be built. The question is whether it can be built before November 10.

Source: USA Rare Earth Serra Verde acquisition — https://www.metaltechnews.com/story/2026/04/22/tech-metals/usa-rare-earth-goes-global-with-28b-deal/2724.html

Source: Clark Hill PLC: China Export Control Suspension Analysis — https://www.clarkhill.com/news-events/news/china-hits-pause-on-rare-earth-export-controls-and-what-it-means-for-supply-chains/

Source: IEA: Supply Concentration Risks Become Reality — https://www.iea.org/commentaries/with-new-export-controls-on-critical-minerals-supply-concentration-risks-become-reality

RESEARCH RADAR

Five Studies and Announcements Worth Your Attention

1. EIA Annual Energy Outlook 2026: 2.1%/Year Electricity Demand Growth After 15 Years of Flat Consumption

U.S. Energy Information Administration | April 8, 2026

The AEO2026 documents a structural inflection point in U.S. electricity consumption: after 15 years of essentially flat demand, consumption has grown 2.1 percent per year on average over the past five years. The compound demand driver is electrification — EVs, heat pumps, industrial electrification — and AI/data center infrastructure. Total installed generating capacity is projected to increase 50 to 90 percent by 2050 depending on policy assumptions. Natural gas generation’s absolute volume increases in all scenarios; coal’s share declines substantially in most.

WHY IT MATTERS: The 2.1 percent annual growth rate, compounded across the 15-year planning horizon, represents an additional demand obligation of approximately 900 billion kilowatt-hours by 2035 — roughly equivalent to the entire current electricity consumption of Germany and France combined. Every percentage point of demand growth that is not matched by new dispatchable capacity additions tightens reserve margins. AEO2026 is the planning foundation document for every energy technology investment decision through the end of the decade.

Source: EIA Annual Energy Outlook 2026 — https://www.eia.gov/outlooks/aeo/

2. EIA STEO April 2026: LNG Exports at 17.9 Bcfd in March (2nd-Highest Record); Full-Year Forecast Raised to 17.0 Bcfd

U.S. Energy Information Administration | April 7, 2026

EIA’s April Short-Term Energy Outlook estimates March 2026 U.S. LNG exports at 17.9 billion cubic feet per day — the second-highest monthly record, 8 percent above the January forecast. The Hormuz LNG supply disruption widening the domestic-to-international price spread is identified as the explicit driver. Full-year 2026 LNG exports are raised to 17.0 Bcfd from 16.4 Bcfd in January. Additional 0.9 Bcfd of nameplate capacity is expected online in 2Q26 from Corpus Christi Stage 3 Train 5 and Golden Pass Train 1 — which shipped its first cargo this week.

WHY IT MATTERS: The Hormuz crisis has demonstrated in real time what the research community has modeled theoretically for years: U.S. LNG export infrastructure is not just commercial infrastructure — it is a strategic national asset whose throughput directly affects allied energy security. The STEO’s above-forecast LNG exports confirm that the spread between domestic and international prices is driving maximum terminal utilization. The DPA natural gas/LNG determination creates the federal procurement mechanism to accelerate the next phase of export capacity expansion.

Source: EIA Short-Term Energy Outlook April 2026 — https://www.eia.gov/outlooks/steo/pdf/steo_full.pdf

3. TIME Magazine: ‘The Sobering Truth About Rare Earths’ — Independent Coverage Documents 94% China Magnet Market Share

TIME Magazine | April 20, 2026

TIME Magazine’s investigative report on rare earth supply chains documents China’s 94 percent share of global permanent magnet production (IEA data), up from 50 percent two decades ago. The article covers Project Vault ($12 billion critical minerals stockpile initiative, February 2026), the FORGE multilateral coordination mechanism, and the CSIS finding that the U.S. lacks the heavy rare earth separation capacity to meet defense demand if Chinese controls tighten. CSIS Director Gracelin Baskaran: ‘China overplayed their hand and that you cannot undo.’

WHY IT MATTERS: TIME’s reach into policy, investment, and institutional audiences that do not regularly read critical minerals trade press makes this piece strategically important for advocacy and communications purposes. The 94 percent magnet market share figure — independently verified by IEA data — is the single most powerful quantitative illustration of the supply chain risk. ERR recommends this piece as a briefing document for policymakers and board-level discussions on critical minerals strategy.

Source: TIME Magazine: The Sobering Truth About Rare Earths — https://time.com/article/2026/04/20/trump-s-push-to-break-china-s-dominance-of-critical-rare-earth-minerals/

4. EIA Weekly Natural Gas Storage (Week Ending April 17): 103 Bcf Injection — 8% Above Seasonal Norms as Henry Hub Falls to $2.52/MMBtu

U.S. Energy Information Administration | Released April 24, 2026

The EIA’s April 24 Weekly Natural Gas Storage Report showed a 103 Bcf injection for the week ending April 17 — above the 77 Bcf injected the same week in 2025 and 39 Bcf above the 64 Bcf five-year average. Working gas in storage is estimated at approximately 2,073 Bcf, approximately 8 percent above seasonal norms. Henry Hub closed at $2.52 per MMBtu on April 24 — the lowest since October 2024, down approximately 19 percent year-over-year. The low price prompted EQT Corporation to curtail Appalachian production, taking Lower 48 dry gas output to an 11-week low of approximately 108.1 Bcfd.

WHY IT MATTERS: The convergence of $2.52/MMBtu Henry Hub with near-record LNG exports at 18.9 Bcfd illustrates the structural asymmetry the Hormuz crisis has created: domestic gas is cheap because production is high and domestic demand is soft in the spring shoulder season, while global LNG markets are running a historic scarcity premium. For energy researchers and technology developers, this is the empirical case for domestic LNG export infrastructure expansion: the domestic resource is abundant, the global demand is acute, and the infrastructure gap between them is exactly what the DPA natural gas/LNG determination is designed to close.

Source: EIA Weekly Natural Gas Storage Report (April 24, 2026) — https://www.eia.gov/naturalgas/storage/

5. OSMRE FY2026 AMLER Funding: $134M to Coal Communities — REE Co-Location Opportunity at Abandoned Mine Sites

Office of Surface Mining Reclamation and Enforcement | April 2026

OSMRE announced $134 million in FY2026 AMLER (Abandoned Mine Land Economic Revitalization) program funding for coal communities in Central Appalachian states — West Virginia, Kentucky, Pennsylvania, and Virginia. AMLER directs abandoned mine land reclamation funds to economic development projects at eligible sites. The Seneca Center’s inventory of more than 80 former surface mine sites in West Virginia — documented as part of the Center’s Appalachian REE research program — identifies sites where AMLER remediation activities can be co-located with REE extraction and critical minerals processing infrastructure.

WHY IT MATTERS: AMLER funding creates an economic co-location framework that addresses two policy objectives simultaneously: legacy environmental liability remediation and critical minerals supply chain development. A former surface mine site receiving AMLER remediation funding has existing road access, disturbed land that limits additional NEPA exposure, and regulatory precedent for industrial activity. The Heritage Critical Minerals/Eureka Energy integrated model — plasma gasification, REE recovery, data center co-location on former Appalachian surface mine sites — is designed precisely for this site profile. The combination of AMLER, CORE-CM, and DPA financing authority creates a three-source federal funding stack for Appalachian REE projects that did not exist simultaneously before this week.

Source: OSMRE AMLER Program / World Coal —

RESEARCH & COMMERCIALIZATION PIPELINE

DOE | NETL | NREL | National Laboratories | University Programs | SBIR/STTR | Technology Transfer

This section tracks project-level developments across the federal energy research and technology development pipeline: NOFO awards, laboratory milestones, SBIR/STTR commercialization advances, technology transfer agreements, and university program developments. ERR’s standing commitment is to follow these projects through from announcement to deployment outcome — not to stop at press release day.

1. NETL Morgantown Coal Center of Excellence: Formally Launched February 2026 — Research Structure for the FY2027 Budget Era

NETL / DOE Hydrocarbons and Geothermal Energy Office | February 2026

The Trump administration formally launched NETL’s Coal Center of Excellence at the Morgantown, WV campus in February 2026, as part of a four-center restructuring of NETL’s research mission: Coal at Morgantown; Oil and Natural Gas at Pittsburgh, PA; Critical Minerals and Advanced Alloys at Albany, OR; and a Geothermal center to be designated. The restructuring is designed to align NETL’s research capabilities with specific industry sectors rather than the cross-cutting program structure of prior administrations. The Morgantown Coal Center’s priority research areas include coal-to-products (graphite, rare earth recovery, advanced materials), coal plant modernization and life-extension, and combustion efficiency improvements. The FY2027 budget request proposes cutting overall NETL research operations 8 percent to approximately $80 million while increasing infrastructure funding 2 percent to $58 million.

WHY IT MATTERS: The Centers of Excellence restructuring signals a lasting reorientation of NETL toward applied, commercial-facing research aligned with the administration’s reliability and energy security priorities. For industry partners and university research teams, the Center structure creates clearer pathways for collaboration and technology transfer than the prior programmatic organization. Researchers seeking NETL partnerships in coal, critical minerals, or geothermal should engage the relevant Center directly rather than through legacy program offices.

Source: NETL Centers of Excellence —

Source: DOE Hydrocarbons and Geothermal Energy Office / Laboratories and Facilities — https://www.energy.gov/hgeo/laboratories-and-facilities

2. DOE FY2027: NREL/National Laboratory of the Rockies Faces 52% Budget Cut ($264M Reduction) — Renewable Research Infrastructure Under Restructuring

DOE / pv magazine USA | April 16, 2026

The DOE FY2027 budget justification proposes a 52 percent funding cut — $264 million — to the National Laboratory of the Rockies (the facility formerly known as NREL, the National Renewable Energy Laboratory in Golden, Colorado). The reduction follows broader federal restructuring that has centralized DOE’s research mission around traditional energy resources, defense applications, and AI computing infrastructure. Energy Secretary Wright has simultaneously proposed that data center developers co-locate facilities on national laboratory property, with computing resources shared between commercial and laboratory uses. NETL itself faces a 32 percent cut ($305 million reduction) from current levels under the same proposal, with elimination of hydrogen, vehicles, bioenergy, transmission, methane mitigation, carbon dioxide removal, carbon utilization, and point-source carbon capture research programs.

WHY IT MATTERS: The proposed cuts are not yet law — Congressional appropriators will have the final word, and House Republicans’ budget austerity push creates political complexity. The cuts that matter most for ERR’s coverage area are the NETL reductions: methane mitigation and point-source carbon capture program elimination would reduce the research pipeline feeding into gas plant efficiency and emissions management technologies. The data center co-location proposal at national labs is a structural innovation worth tracking — Wright has specifically mentioned next-generation nuclear reactor testing on federal lands as part of the same initiative.

Source: pv magazine USA: Trump DOE Proposes 52% Budget Cut for National Laboratory of the Rockies — https://pv-magazine-usa.com/2026/04/16/trump-doe-proposes-52-budget-cut-for-national-laboratory-of-the-rockies/

3. NETL/Argonne BLAZE Center: $10M Award for Industrial Combustion Research — Flexible Fueling for Refineries and Chemical Plants

NETL / DOE Industrial Technologies Office | 2026

The DOE Industrial Technologies Office selected NETL and its partners at Argonne National Laboratory (ANL) to receive $10 million in funding to develop the Burner Laboratories to Advance fuel utiliZation for thermal Energy (BLAZE) Center. The BLAZE Center is designed to advance industrial burner technologies that enable refineries, chemical processing facilities, and other energy-intensive manufacturers to use diverse fuel blends — including mixed natural gas, hydrogen, and biomass-derived gas streams — while meeting strict NOx and emissions limits without post-combustion control systems. The program connects directly to ClearSign Technologies Corporation’s NETL-supported SBIR Phase II project, which is preparing field demonstrations of flexible industrial burner technology at operational refinery and chemical plant sites.

WHY IT MATTERS: Industrial fuel flexibility is increasingly critical as gas price volatility, the Hormuz supply disruption, and the hydrogen policy debate all create operational uncertainty for energy-intensive manufacturers. The ability to switch between fuel types without retooling combustion systems reduces energy cost exposure and supply chain risk for the refining, chemicals, and advanced manufacturing sectors. BLAZE represents exactly the class of applied industrial research that ERR tracks: SBIR-funded, commercially-oriented, approaching field demonstration rather than laboratory proof-of-concept.

Source: NETL News Room — BLAZE Center Award — https://www.netl.doe.gov/news-room-news-stories

Source: NETL Partner Project: ClearSign Low-NOx Flexible Fueling — https://netl.doe.gov/node/15305

4. NETL Critical Minerals Matchmaker (CM3) Survey Results Released — Connecting Supply Chain Gaps to Research Capabilities

NETL | April 2026

NETL released insights from its Critical Minerals and Materials Matchmaker (CM3) survey, an online information resource created to identify and bridge gaps between industry supply chain needs and federal research capabilities across the critical minerals and materials value chain. The CM3 survey maps specific mineral processing, separation, and materials manufacturing needs against the research programs, facilities, and team capabilities at NETL and partner institutions. It is designed to accelerate the connection between private sector developers with specific technology gaps and the federal laboratory resources that can address them. The survey is a companion tool to the ClaiMM digital platform (launched January 23, 2026) and the METALLIC multi-lab critical minerals infrastructure ($75M, 9 national labs led by NETL).

WHY IT MATTERS: The CM3 survey and ClaiMM platform represent the data infrastructure layer of the federal critical minerals strategy — less visible than billion-dollar investment announcements but potentially more impactful for the project developers who actually need to close specific technology gaps. A company developing an Appalachian REE extraction process that needs specific separation chemistry expertise can now find the relevant NETL team through CM3 rather than navigating the federal contracting process blind. ERR will monitor the CM3/ClaiMM pipeline for evidence that it is accelerating project-to-commercialization timelines.

Source: NETL Critical Minerals Matchmaker Survey Results — https://netl.doe.gov/news-room-news-stories

5. NETL Utah FORGE Geothermal: Enhanced Geothermal Systems Field Operations Complete — Commercial Pathway Identified

NETL / DOE Geothermal Technologies Office / University of Utah EGI | Ongoing through 2026

The Utah Frontier Observatory for Research in Geothermal Energy (Utah FORGE), located on the western flank of the Mineral Mountains, has completed its current-phase field operations with NETL support. The project — a partnership between NETL, DOE’s Geothermal Technologies Office, and the Energy and Geoscience Institute at the University of Utah — has demonstrated successful enhanced geothermal systems (EGS) technology applicable to sites without conventional hydrothermal resources. Key technical achievements: successful hydraulic fracturing in hot dry rock at depth, demonstration of fluid injection and recovery pathways, and characterization of the thermal reservoir performance that provides the economic modeling foundation for commercial EGS projects. The FY2027 budget proposes increasing geothermal funding at DOE headquarters and NREL while cutting Lawrence Berkeley and Sandia geothermal programs.

WHY IT MATTERS: Enhanced geothermal systems are the only dispatchable renewable electricity generation technology with the geographic distribution and baseload capability to meaningfully supplement coal and gas as the fleet transitions. Utah FORGE’s field completion demonstrates that EGS is technically achievable outside traditional western hydrothermal zones — which matters because most U.S. electricity load centers are not in traditional geothermal areas. A commercially replicable EGS pathway would be the most significant reliability-relevant renewable energy technology development in decades. ERR will track the commercialization transition from FORGE field data to private-sector FID decisions.

Source: NETL Utah FORGE Project — https://netl.doe.gov/node/13952

Source: NETL: Geothermal Breakthrough Research Results — https://netl.doe.gov/node/11465

6. NETL/DOE NOFO: Coal Plant Efficiency, Reliability, and Flexibility — Advanced Wastewater Management and System Optimization

NETL eXCHANGE (DE-FOA-0003607) | January-April 2026

NETL issued a Notice of Intent (DE-FOA-0003607) followed by a full NOFO for projects advancing efficiency, reliability, and flexibility at coal-based power plants, with a specific focus on advanced wastewater management systems. The NOFO objectives target development of advanced wastewater management technologies for coal plant operations — addressing one of the most significant operational cost and regulatory compliance challenges for plants seeking to extend their useful lives. The application deadline for the full NOFO was January 2026; awards are expected in the 2026 timeframe. The program connects directly to the $175 million DOE coal plant modernization awards announced February 12, 2026 (Mountaineer and Amos plants in WV; Cardinal in OH; Belews Creek in NC; Ghent in KY; Fort Martin in WV; Kyger Creek in OH).

WHY IT MATTERS: Wastewater management has emerged as a primary operational constraint for coal plants seeking life-extension under DOE emergency orders — plants that have not upgraded wastewater systems to current EPA standards face regulatory pressure that independent of the FPA 202(c) order framework. NETL’s targeted NOFO for wastewater management technology development addresses a specific, commercially real bottleneck in the plant modernization pipeline. Companies with coal plant clients should monitor award announcements for potential technology partnership opportunities.

Source: NETL eXCHANGE: DE-FOA-0003607 Coal Plant Flexibility —

https://netl-exchange.energy.gov/

Source: DOE $175M Coal Plant Modernization Awards (February 12, 2026) — https://netl.doe.gov/node/15267

7. DOE ‘Genesis Mission’: Secretary Wright Announces AI Computing Infrastructure on National Lab Property — Nuclear Reactor Testing on Federal Lands

DOE / E&E News | April 2026

Energy Secretary Chris Wright announced the ‘Genesis Mission’ initiative to transform American science and innovation through AI computing infrastructure, including specific proposals to co-locate data center facilities on national laboratory property. At NETL in Morgantown, Wright stated: ‘You will see data centers built on national lab property. You will also see next-generation nuclear reactors tested on federal lands sometime next year.’ The proposal would share computing capacity between commercial hyperscale data center operators and DOE national laboratory research teams, with the commercial data center revenue partially offsetting laboratory operating costs. The initiative connects to the broader energy demand surge from AI infrastructure and the administration’s push to commercialize next-generation nuclear through federal land availability.

WHY IT MATTERS: The Genesis Mission proposal represents a novel public-private partnership model for national laboratory financing that, if implemented, would change the economic structure of federal research infrastructure. Data center developers gain access to federal land, transmission infrastructure, and regulatory streamlining; national laboratories gain computing capacity and a revenue stream at a time when federal appropriations are under pressure. Wright’s specific mention of next-generation nuclear reactor testing on federal lands is the most significant signal yet that the administration intends to use DOE’s land authority as a primary lever for accelerating advanced nuclear commercialization.

Source: E&E News: How Chris Wright is Remaking the National Labs — https://www.eenews.net/articles/how-chris-wright-is-remaking-the-national-labs/

Source: NETL: Energy Department Launches Genesis Mission —

About This Publication

Energy Research Review is published weekly on Mondays by The Hedley Company, a strategic communications and energy policy consultancy based in Charleston, W.Va. Content covers federal energy research, national laboratory activity, technology commercialization, regulatory and policy developments, and funding intelligence across the full energy sector. All sources are verified. Live URLs are required on all cited items. ERR does not accept advertising and operates under no commercial arrangement with any source cited herein.

AI assistance was used in research and drafting under the author’s direction and editorial control, consistent with specialized research software. All judgments and conclusions are the author’s own.

By T.L. Headley, MBA | President, The Hedley Company | Charleston, W.Va.