A Publication of The Hedley Company: Communications and Research for Energy

Feb 14, 2026

∙ Paid

EXECUTIVE SUMMARY

This weekly report synthesizes key developments across U.S. coal production, electric power generation and demand, steel manufacturing, and rail transportation. The analysis reflects data released the week of February 9–14, 2026 and captures the operational rebound following Winter Storm Fern, alongside the landmark week in energy policy that saw President Trump rescind the EPA’s 2009 CO₂ endangerment finding — the most consequential deregulatory action in American energy history.

Production and transportation logistics recovered materially this week after the weather-driven disruptions of the prior period, while coal spot prices firmed across all major regions. The policy environment shifted dramatically in coal’s favor, with the endangerment finding rescission eliminating the foundational regulatory burden that had driven premature plant retirements across the nation.

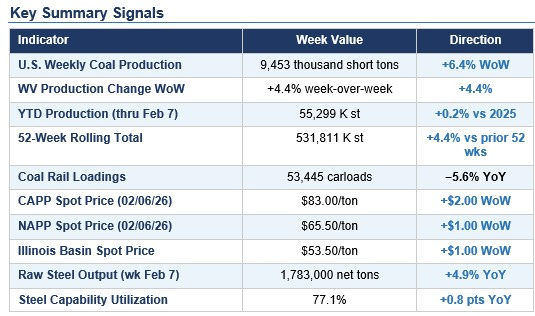

Key Summary Signals

Overall insight: The week ending February 7, 2026 marks a decisive inflection on two dimensions simultaneously — operationally, with a strong production rebound and firming prices across all major coal regions; and politically, with the Trump administration delivering on its most significant energy deregulatory promise. The dual dynamic of operational recovery and regulatory relief creates the most favorable short-term environment for U.S. coal since 2022.

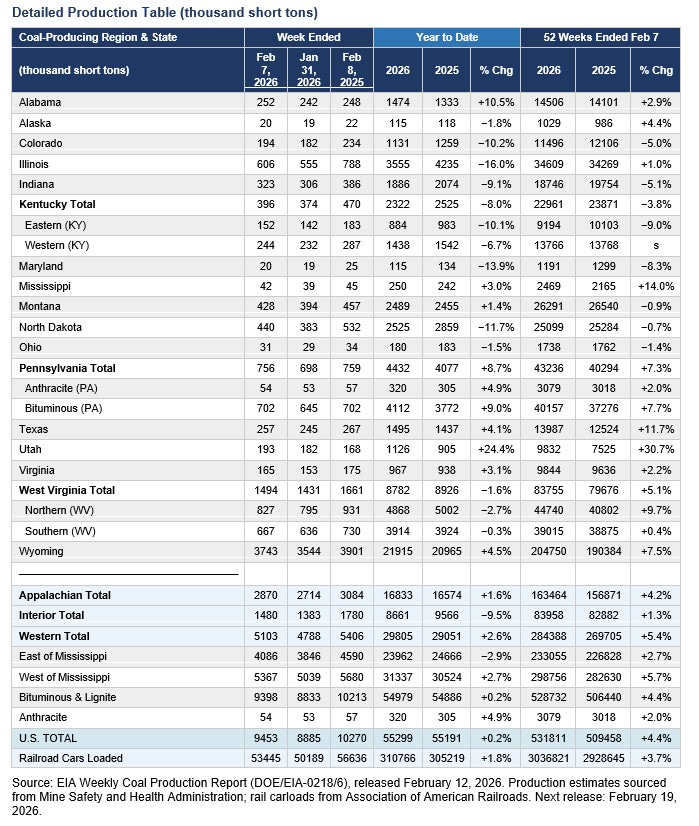

SECTION 1 — U.S. Coal Production Report

Week Ending February 7, 2026 | EIA Weekly Coal Production Report (DOE/EIA-0218/6), Released February 12, 2026

National Overview

Total U.S. coal production for the week ending February 7, 2026, was 9,453 thousand short tons — up 6.4% from the prior week’s storm-depressed 8,885 thousand short tons, but still 7.9% below the 10,270 thousand short tons produced in the comparable week last year. The week-over-week rebound reflects logistics normalization following Winter Storm Fern, with most major producing regions posting meaningful gains.

West Virginia rebounded to 1,494 thousand short tons, up 4.4% from 1,431 the prior week. Wyoming recovered to 3,743 thousand short tons, up 5.6% from 3,544. Pennsylvania strengthened to 756 thousand short tons, up 8.3%. Notably, Utah continued its exceptional trajectory, posting 193 thousand short tons — up 6.0% WoW and +15.5% YoY, extending its remarkable 52-week gain of +30.7%, the strongest of any producing state in the nation.

Year-to-date production through February 7 stands at 55,299 thousand short tons, barely ahead (+0.2%) of the same period in 2025, reflecting the cumulative impact of the storm week disruption. The 52-week rolling total of 531,811 thousand short tons remains solidly ahead of the prior year at +4.4%, confirming the underlying positive production trend.

Detailed Production Table (thousand short tons)

Source: EIA Weekly Coal Production Report (DOE/EIA-0218/6), released February 12, 2026. Production estimates from MSHA; rail carloads from AAR. Next release: February 19, 2026. s = Value less than 0.5 of table metric but included in totals.

Regional Highlights

Appalachian Total: 2,870 K st — up +5.7% WoW from 2,714; YTD +1.6% vs. 2025; 52-week +4.2%. Recovery led by Pennsylvania bituminous (+8.9% WoW) and WV Northern district (+4.0% WoW).

Interior Total: 1,480 K st — up +7.0% WoW but YTD still −9.5% vs. 2025. Illinois remains the region’s primary drag at −16.0% YTD, reflecting ongoing structural demand shifts for its high-sulfur thermal product.

Western Total: 5,103 K st — up +6.6% WoW; YTD +2.6%; 52-week +5.4%. Wyoming’s rebound anchors the region. Utah continues to outperform with +24.4% YTD gain.

Utah standout: 193 K st this week; YTD +24.4% and 52-week +30.7% — strongest growth trajectory of any producing state, driven by export demand and retained utility contracts.

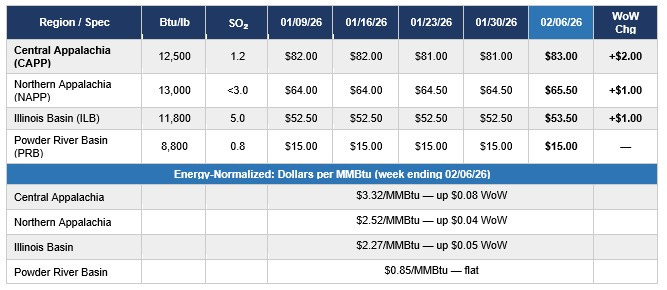

SECTION 2 — U.S. Coal Spot Prices

Week Ending February 6, 2026 | EIA Coal Markets Report, Released February 9, 2026

Spot prices strengthened across all major coal-producing regions for the week ending February 6, 2026, marking the first broad-based price increase since November 2025. Central Appalachian thermal coal gained $2.00 to $83.00/ton, Northern Appalachia gained $1.00 to $65.50/ton, and Illinois Basin added $1.00 to $53.50/ton. Powder River Basin remained flat at $15.00/ton. On an energy-normalized basis, CAPP advanced to $3.32/MMBtu, its highest level since October 2025.

Spot Prices — Dollars per Short Ton (Prompt Quarter Delivery)

Energy-Normalized — Dollars per MMBtu (Week Ending 02/06/26)

Region$/MMBtuWoW ChangeCentral Appalachia$3.32/MMBtu+$0.08Northern Appalachia$2.52/MMBtu+$0.04Illinois Basin$2.27/MMBtu+$0.05Powder River Basin$0.85/MMBtuflat

Source: EIA Coal Markets Report (S&P Global data), released February 9, 2026. Prices reflect prompt quarter delivery. NYMEX coal futures: consult CME Group. Uinta Basin series discontinued April 30, 2024.

The firming reflects tight post-storm supply conditions, increased utility stock-rebuilding demand, and improving export market dynamics driven by Indonesian production restrictions. The strengthening is broad-based and represents the first meaningful price catalyst in three months.

SECTION 3 — Electricity Generation, Demand & Grid Update

Week of February 8–14, 2026 | EIA Hourly Electric Grid Monitor; EIA STEO February 2026

As grid conditions normalized following Winter Storm Fern, coal-fired generation moderated from its storm-peak of approximately 21% national share back toward its baseline of 18–19%, with natural gas reassuming its dominant position. February’s moderate temperatures allowed generation reserves to rebuild across PJM, MISO, and SERC.

EIA’s February 2026 Short-Term Energy Outlook (released February 10) projects U.S. coal generation to average 194 billion kilowatthours in Q1 2026, up from 181 BkWh in Q1 2025 — a 7.2% year-over-year increase — driven by higher natural gas prices and retained coal capacity under DOE 202(c) emergency orders. The rescission of the CO₂ endangerment finding on February 12 further removes the regulatory ceiling that had been suppressing coal generation investment.

PJM: Demand normalizing post-storm; reserve margins improving. J.H. Campbell (Michigan) retention litigation ongoing; Consumers Energy citing $600K/day in operating costs.

MISO: Post-storm logistics recovery underway; coal stockpile rebuilding across Midwest utilities expected to support sustained dispatch through March.

ERCOT/SPP: Moderate conditions; natural gas dominant with coal providing baseload complement. No emergency conditions reported.

National generation share (normalized week): Coal ~18–19%; natural gas ~37–39%; nuclear ~19%; wind ~11–12%; solar ~5%.

SECTION 4 — U.S. Steel Production & Demand

Week Ending February 7, 2026 | AISI Weekly Raw Steel Production Report, Released February 11, 2026

U.S. raw steel production surged to 1,783,000 net tons for the week ending February 7 — the highest weekly output in five months — up 1.4% from the prior week’s 1,758,000 net tons and up a strong 4.9% from 1,700,000 net tons in the same week of 2025. Capacity utilization climbed to 77.1%, up from 76.0% the prior week.

Year-to-date production through February 7 reached 9,557,000 net tons, up 3.7% year-over-year. By district: Northeast 124K tons; Great Lakes 526K tons; Midwest 269K tons; South 800K tons; West 64K tons.

Warrior Met Coal’s Q4 2025 earnings (released February 12) confirmed record sales volumes and net income of $23.0 million (up 1,991% YoY), with 2026 guidance of 12.5–13.5 million short tons — approximately 30% above 2025 levels — reflecting the full-year contribution of the Blue Creek No. 1 longwall mine. Alabama BLM federal coal lease awards this week provide Warrior Met with access to 53 million additional tons on 14,050 acres of federal mineral estate.

SECTION 5 — U.S. Coal Employment & Economic Footprint

February 2026 Estimate | BLS CES Series CES1021210001; IBISWorld

Direct coal mining employment remains at approximately 40,700 workers (BLS December 2025 baseline). Applying the industry-standard 3.5× indirect employment multiplier, the total U.S. coal industry employment footprint is estimated at approximately 183,150 jobs generating roughly $11.5 billion in annual wages.

The administration’s DOE $625 million investment initiative for coal industry modernization — announced this week — is specifically designed to support coal communities, upgrade plant capabilities, and provide economic transition support for coal-dependent regions. Combined with the endangerment finding rescission and expanded federal land access, the week’s policy actions represent the most comprehensive federal commitment to coal communities since the Appalachian Regional Commission’s founding generation.

SECTION 6 — Rail & Barge Transportation

Week Ending February 7, 2026 | AAR Weekly Rail Traffic, Released February 11, 2026

U.S. rail traffic for the week ending February 7, 2026 totaled 486,854 carloads and intermodal units, down 3.2% year-over-year but recovering sharply from the storm-week low of 434,361. Total carloads came in at 208,408, down 4.8% YoY, while intermodal volume was 278,446 units, down 2.0% YoY.

Coal carloads recovered to 53,445 — up from 50,189 the prior week (+6.5% WoW) but still down 3,540 carloads (−6.2%) versus the same week in 2025 at 56,985. Year-to-date through five weeks of 2026, total U.S. rail carloads are up 2.5% from the same period last year, led by grain, petroleum products, and motor vehicles.

Barge conditions on the Illinois River system are reported to be recovering as ice conditions moderate, with normal operations expected to resume on key Midwest waterway corridors by mid-February.

SECTION 7 — Domestic News: Top 10 Coal Industry Headlines

Week of February 9–14, 2026

1. Trump Rescinds EPA CO₂ Endangerment Finding in Historic Deregulatory Action NPR / NBC News / AP | February 12, 2026

President Trump and EPA Administrator Lee Zeldin formally rescinded the Obama-era 2009 CO₂ endangerment finding, eliminating the legal foundation for greenhouse gas regulation under the Clean Air Act. Zeldin described it as “the largest deregulatory action in American history,” projected to save $1.3 trillion in regulatory costs. Interior Secretary Burgum framed the action as directly enabling “the revival of clean, beautiful American coal.”

Why It Matters: The rescission removes the keystone regulatory burden that has driven premature coal plant retirements, blocked investment, and increased electricity costs for American families for 16 years. Legal challenges are expected from environmental groups and state attorneys general, but the action immediately changes the investment calculus for every coal plant still operating in the United States.

2. Trump Signs ‘Clean Beautiful Coal’ Executive Order Directing DoD to Prioritize Coal-Fired Power Christian Science Monitor / AP | February 11–12, 2026

President Trump signed an executive order directing the Department of Defense to prioritize long-term on-demand power purchase agreements with coal-based power plants for military installations, positioning national security as a direct rationale for sustained coal generation investment.

Why It Matters: A DoD procurement anchor for coal-fired power creates durable federal demand insulated from commercial market cycles, providing investment certainty for retained plants and potentially supporting new or upgraded capacity at military-adjacent locations.

3. Warrior Met Coal Reports Record 2025 Production; Blue Creek at Full Ramp; Projects 30%+ Volume Growth in 2026 Yahoo Finance / Warrior Met Coal | February 12, 2026

Warrior Met Coal released Q4 2025 earnings showing net income surged 1,991% year-over-year to $23.0 million, with record production and sales volumes for both Q4 and full year 2025. CEO Walt Scheller highlighted the ahead-of-schedule Blue Creek No. 1 longwall ramp-up, which achieved a 1.5 million short ton quarterly run rate. 2026 guidance calls for coal sales of 12.5–13.5 million short tons.

Why It Matters: Blue Creek’s expansion makes Warrior Met one of the largest and lowest-cost met coal producers in the Western Hemisphere. The scale-up directly supports U.S. metallurgical coal export competitiveness at a time when global benchmark prices are near one-year highs.

4. BLM Alabama Coal Lease Auction Generates $46M, Unlocks 53 Million Tons for Warrior Met World Coal / Interior Dept. | Week of February 9, 2026

The Department of the Interior announced that a Bureau of Land Management competitive coal lease sale in Tuscaloosa County, Alabama generated over $46 million in revenue and grants access to 53 million tons of metallurgical coal on 14,050 acres of federal mineral estate, directly benefiting Warrior Met Coal’s Blue Creek expansion.

Why It Matters: The lease award extends Warrior Met’s reserve base significantly, supporting decades of high-quality metallurgical coal production from Alabama’s premier coking coal district and reinforcing U.S. met coal export market position.

5. DOE Announces $625 Million Investment to Expand and Reinvigorate U.S. Coal Industry World Coal / DOE | Week of February 9, 2026

The U.S. Department of Energy announced a $625 million investment initiative targeting coal production capacity, community support, and technology upgrades — signaling sustained federal financial commitment alongside the regulatory relief provided by the endangerment finding rescission.

Why It Matters: Federal capital investment combined with deregulatory action represents a two-pronged strategy addressing both the structural financial constraints on coal operators and the regulatory barriers that have made investment uneconomic — the most comprehensive federal coal support in a generation.

6. Bloomberg: J.H. Campbell Retention Costs $600K/Day; Consumers Energy May Pass to Ratepayers Bloomberg | February 14, 2026

Bloomberg published a critical investigation of the J.H. Campbell coal plant retention in Michigan, reporting Consumers Energy cites $600,000 per day in operating costs for the federally mandated extension, with potential ratepayer cost pass-through.

Why It Matters: The Bloomberg narrative represents the emerging media and political counter-offensive to coal retention policy. The substantive rebuttal: coal supplied 24% of peak generation during Winter Storm Fern, and the systematic underpricing of that reliability in current market structures is the critical missing context in cost-per-day framing.

7. EIA February STEO: Coal Generation Up 7.2% YoY in Q1 2026; Full-Year Production Forecast Remains Challenged EIA Short-Term Energy Outlook | February 10, 2026

EIA’s February STEO projects U.S. coal generation to average 194 BkWh in Q1 2026, up 7.2% from Q1 2025. However, full-year 2026 coal production and consumption are still projected to decline 2.2% and 4.7%, respectively, from 2025 levels.

Why It Matters: The STEO confirms near-term generation gains from retained capacity and gas price dynamics, but the full-year decline projection underscores that emergency orders and deregulation must be followed by sustained market structure reform to reverse the structural production trajectory.

8. EPA Extends Coal Ash Cleanup Deadlines to 2031–2032 in Companion Deregulatory Action Utility Dive / Earthjustice | February 10, 2026

EPA issued a final rule extending compliance deadlines for groundwater monitoring and investigation at legacy coal ash impoundments to February 2031–2032, providing operational cost relief for coal plant operators retaining capacity under emergency orders.

Why It Matters: Near-term reduction in coal ash compliance costs directly improves the economics of plant retention, supporting the administration’s grid reliability strategy by reducing the regulatory burden that has made some plants uneconomic to operate even when technically capable.

9. Coal Age 2026 U.S. Longwall Census: 36 Active Faces; Warrior Met Blue Creek Debuts; Core Natural Resources Restarts Leer South Coal Age | Week of February 9, 2026

Coal Age’s annual U.S. Longwall Census reports 36 active longwall faces for 2026, with Warrior Met’s Blue Creek No. 1 added and Core Natural Resources restarting the idled Leer South longwall in West Virginia.

Why It Matters: The addition of Blue Creek and restart of Leer South represent meaningful capital redeployment into Appalachian met coal production — a direct indicator of investor confidence in the coal sector’s near-term commercial viability.

10. Global Thermal Coal Benchmark Hits One-Year High Above $115/ton; Indonesian Supply Restrictions Support Prices Trading Economics / Argus Media | February 9–14, 2026

Global thermal coal benchmarks exceeded $115 per metric ton during the week, driven by strong Asian power generation demand (particularly AI data center load growth in China), Indonesian export restriction uncertainty, and tight European supply.

Why It Matters: Elevated global benchmark prices improve the economics of U.S. thermal and metallurgical coal exports, particularly for Appalachian producers shipping through Atlantic ports. Indonesian supply restriction uncertainty creates additional upside risk for U.S. exporters with established Asian market relationships.

SECTION 8 — International Coal Industry Headlines

Week of February 9–14, 2026

1. Global Coal Benchmark Tops $115/ton — One-Year High on AI Demand and Indonesia Supply Fears Trading Economics / Argus | February 9–14, 2026

Newcastle thermal coal benchmark exceeded $115/ton this week, driven by power generation demand from AI data centers, Indonesia’s production restriction moves, and Chinese restocking needs heading into spring. The 8% monthly gain and 9.6% YoY increase mark the strongest price environment since early 2025.

Why It Matters: High global benchmarks underpin U.S. thermal export margins and provide pricing support for Appalachian producers, creating favorable conditions for increased export volume.

2. IEA Electricity 2026 Report: Global Power Demand to Grow 3%+ Per Year; Coal Share Erodes Despite Rising Volume Argus Media / IEA | February 9, 2026

The IEA’s Electricity 2026 report projects global power demand growth exceeding 3% annually through 2030, driven by electrification, AI data centers, and EV charging. While coal consumption volumes may hold near current levels in absolute terms, its share of the global generation mix is projected to erode.

Why It Matters: The IEA framework is increasingly used by international lenders and ratings agencies to assess coal asset risk. U.S. coal operators with strong domestic market positions and export diversification are best positioned regardless of IEA share projections.

3. Indonesia Supply Restriction Uncertainty Roils Asian Coal Markets; Force Majeure Declared by Major Sumatra Producer Argus Media | February 6–9, 2026

Indonesia’s energy ministry is still finalizing 2026 output quotas, creating market uncertainty. A major Sumatra-based producer declared force majeure on shipments, contributing to the sharp benchmark rally. Indonesia targets output cuts to ~600 million tons from ~800 million tons in 2025.

Why It Matters: Supply disruptions from the world’s largest thermal exporter directly benefit U.S. Appalachian and Illinois Basin producers with existing Asian customer relationships, creating an export opening that could partially offset domestic demand pressures.

4. China Coal Production to Grow at Slowest Pace This Decade in 2026; Imports Forecast to Fall 5.1% World Energy News / CCTD | February 10–11, 2026

China’s Coal Transportation and Distribution Association projects 2026 domestic production at 4.86 billion tons (+0.7%, slowest pace this decade) while imports are forecast to fall 5.1% to 465 million tons.

Why It Matters: Slower Chinese import growth tempers the most optimistic scenarios for U.S. thermal coal export expansion to Asia, but the Indonesian supply gap creates selective opportunities for producers able to offer reliable, quality-certified product.

5. Russia’s Kemerovo Coal Crisis Deepens: Mine Ventilation Failures, Industry Bankruptcies Expected in 2026 Moscow Times | February 12, 2026

Russia’s Kemerovo coal region is facing deepening socioeconomic crisis with multiple mine ventilation failures forcing evacuations, widespread industry financial distress, and predictions of dozens of mine bankruptcies in 2026.

Why It Matters: Russian coal industry distress reduces a significant source of seaborne supply competition, particularly for European buyers — benefiting U.S. metallurgical coal exporters who can compete on quality and reliability.

6. Australian Queensland Flooding Disrupts Met Coal Supply; Coking Coal Benchmarks Firm Above $250/mt Coal Hub / Argus | Week of February 9, 2026

Queensland flood-related mining disruptions continued to support Australian premium hard coking coal prices above $250/metric ton fob, with sustained Indian steelmaker demand providing additional upside.

Why It Matters: Premium met coal pricing above $250/mt represents exceptional export margin territory for Alabama and Virginia producers. Every week of sustained elevated prices generates material cash flow improvements for U.S. met coal exporters.

7. Czech Republic Confirms Final Hard Coal Mine Closure by End of 2026 Energies Media | Week of February 9, 2026

The Czech government confirmed it will close the country’s last active hard coal mine by year-end 2026, ending centuries of coal mining in the region and aligning with EU decarbonization commitments.

Why It Matters: European coal phase-outs reduce seaborne thermal coal import demand from traditional Atlantic basin buyers, accelerating the global shift of remaining thermal coal trade toward Asian markets.

8. NRW Holdings’ Golding Contractors Signs New MSA with TEC Coal in Australia World Coal | Week of February 9, 2026

NRW Holdings’ mining services subsidiary Golding Contractors signed a new mining services agreement with TEC Coal in Australia, indicating continued investment in Australian coal mining contract services.

Why It Matters: Continued mining services investment signals institutional capital still views the Australian coal sector as commercially viable — a relevant benchmark for assessing the longer-term durability of global met and thermal coal demand.

9. Tata International and Mercuria Form Coal and Commodities JV for Asian Market Expansion Argus Media | February 6, 2026

Indian commodities trader Tata International and Swiss trading firm Mercuria formed a joint venture focused on coal, metals, and agricultural commodity trade targeting Asian energy and metals supply chains.

Why It Matters: Trading firm positioning in Asian commodity markets indicates continued commercial confidence in thermal and metallurgical coal trade flows to South and Southeast Asia — a positive signal for U.S. Appalachian export market development.

10. China Proposes Record 161 GW of New Coal Power Plants in 2025 — Stranded Asset Risk Flagged Petromindo / CREA | Week of February 9, 2026

China saw a record 161 GW of new coal power plant proposals in 2025, raising stranded asset concerns even as solar capacity is set to surpass coal installed capacity in 2026. The paradox reflects China’s dual-track energy security strategy.

Why It Matters: China’s coal capacity paradox has complex implications: excess domestic capacity could eventually suppress import needs, but near-term sustained demand is supporting global benchmarks at levels favorable to U.S. exporters.

SECTION 9 — Weekly Legislative, Regulatory & Judicial Update

Week of February 9–14, 2026

EPA Rescinds CO₂ Endangerment Finding — The Largest Deregulatory Action in U.S. History

On February 12, 2026, EPA Administrator Lee Zeldin formally finalized the rescission of the 2009 CO₂ endangerment finding alongside President Trump, simultaneously repealing EPA vehicle greenhouse gas emissions standards for light-, medium- and heavy-duty vehicles. The White House projects $1.3 trillion in regulatory cost savings.

Environmental groups including the NRDC, American Lung Association, and American Public Health Association immediately announced legal challenges. The U.S. Climate Alliance called the repeal “unlawful.” The action is expected to trigger years of federal court litigation, with potential Supreme Court review.

Why It Matters: This is the single most consequential regulatory action affecting the coal industry in the 21st century. By removing the legal foundation for CO₂ regulation under the Clean Air Act, it eliminates the primary mechanism through which EPA and future administrations could mandate further coal plant retirements on climate grounds. The litigation timeline means operational certainty for retained plants extends meaningfully, supporting investment and maintenance decisions that would otherwise have been deferred.

Trump Signs Executive Order Directing DoD Coal-Fired Power Procurement

President Trump signed an executive order at the “Clean Beautiful Coal” White House event directing the Department of Defense to prioritize long-term power purchase agreements with coal-based generation assets for military installations. Interior Secretary Burgum stated “CO₂ was never a pollutant” and framed the action as enabling coal’s commercial revival.

Why It Matters: DoD procurement represents a stable, long-term demand anchor insulated from competitive electricity market volatility. Military installations require 24/7 dispatchable power — precisely coal’s core comparative advantage.

EPA Extends Coal Ash Cleanup Deadlines to 2031–2032

EPA’s final rule published February 10 extends groundwater monitoring requirements at legacy coal ash sites to February 2031 (from May 2028) and initial cleanup obligations to February 2032. The rule applies to inactive coal ash ponds, landfills, and impoundments at coal-fired power plants.

Why It Matters: The extension reduces near-term operating cost burdens for utilities retaining coal plants under 202(c) emergency orders, improving the economic case for continued operation.

Ongoing 202(c) Litigation: J.H. Campbell (Michigan), Craig Station (Colorado), Indiana & Washington

Multiple federal court proceedings continue challenging DOE’s use of Federal Power Act Section 202(c) emergency authority. The J.H. Campbell plant received its third extension (to February 17, 2026), with EDF, Sierra Club, and state attorneys general alleging illegality. Consumers Energy reported $600K/day in operating costs for the retained Michigan unit.

Why It Matters: The endangerment finding rescission addresses the underlying regulatory driver of plant closures, potentially reducing the need for further emergency orders — and with it, the litigation exposure.

Federal Judge Upholds Investor ESG Speech; Texas Anti-Fossil Fuel Divestment Law Struck Down

U.S. District Judge Alan Albright ruled Texas’s S.B. 13 — which barred state pension fund investments in firms “boycotting” fossil fuels — unconstitutional under the First and Fourteenth Amendments.

Why It Matters: The ruling protects investor speech broadly on fossil fuel exposure, limiting government overreach into capital allocation decisions and setting precedent that constrains states’ ability to compel pro-fossil fuel investment through pension fund mandates.

SECTION 10 — Weekly SWOT: U.S. Coal Industry Outlook

Week of February 14–21, 2026

STRENGTHS

Production rebounds +6.4% WoW to 9,453 K st — strongest week since December

WV output recovers +4.4% WoW; 52-week rolling total +4.4% YoY at 531,811 K st

Spot prices firm across all regions: CAPP +$2.00 to $83.00/ton, NAPP +$1.00 to $65.50/ton, ILB +$1.00 to $53.50/ton

Steel production reaches 5-month high: 1,783,000 net tons, +4.9% YoY; capacity utilization 77.1%

Rail car loadings recover to 53,445 — up +6.5% WoW from 50,189

EPA endangerment finding rescission removes single largest regulatory threat to coal fleet

Trump Clean Beautiful Coal EO directs DoD to prioritize coal-fired power for military installations

Warrior Met Blue Creek mine at full ramp — record 2025 production; 2026 guidance 12.5–13.5M short tons

Global coal benchmarks reach one-year highs above $115/ton on strong AI data center demand

WEAKNESSES

YTD production barely positive: +0.2% vs. 2025 through Feb 7 — post-Fern disruption still evident in cumulative figures

Coal rail carloads still −5.6% YoY at 53,445 — logistics recovery lagging production rebound

Interior region output remains depressed: −9.5% YTD vs. 2025; Illinois −16% YoY for the week

202(c) litigation risk persists — courts in Michigan, Colorado, Indiana still reviewing DOE authority

Direct coal employment structurally constrained at ~40,700 — production growth faces workforce pipeline limits

PRB spot price flat at $15.00/ton — no improvement despite national production rebound

OPPORTUNITIES

Endangerment finding rescission eliminates CO₂ regulatory ceiling — opens path to investment in retained and upgraded plants

DoD coal procurement EO creates durable federal demand anchor for coal-fired generation

Indonesian output restriction (600M vs. 800M ton target) tightening global thermal supply — opens Asian export lanes

Global benchmark at $115+/ton supports improved U.S. export margins, particularly Appalachian metallurgical grades

Steel at 5-month high with +3.7% YTD output — sustained met coal demand from domestic blast furnace operations

Warrior Met Blue Creek expansion + BLM Alabama lease awards extend U.S. met coal reserve base

Natural gas prices softening into spring — coal dispatch competitiveness improves in marginal hours

DOE $625M investment initiative for coal industry modernization signals continued federal commitment

THREATS

Legal challenges to 202(c) emergency orders create uncertainty for plant retention timeline

Environmental groups and 24 state attorneys general preparing legal challenges to endangerment finding rescission — years of litigation likely

Global seaborne coal trade structurally constrained: European phase-out accelerating; China domestic output growing to 4.86B tons in 2026

EIA forecast: U.S. coal production −2.2% and consumption −4.7% in 2026 — structural headwinds persist despite short-term policy gains

Gas and renewable competition continues suppressing new coal investment and constraining producer access to capital

IEA Electricity 2026 report projects coal share of global generation mix will erode despite rising total demand

Bloomberg narrative on J.H. Campbell ($600K/day) building ratepayer cost-of-coal storyline — requires sustained factual rebuttal

Strategic Note: The week ending February 14, 2026 will be remembered as a historic inflection point for the U.S. coal industry. The simultaneous convergence of production recovery, price firming, the endangerment finding rescission, the DoD coal procurement EO, record met coal output from Warrior Met, and global benchmark prices at one-year highs creates the most favorable short-term environment for coal in years. The critical question for operators and investors is whether these conditions can be converted into durable commercial gains — through plant investment, workforce development, and export market expansion — before the anticipated legal challenges to the rescission create new uncertainty. The window is open. The industry must move.

ANALYSIS: The Keystone Is Out — Now the Real Work Begins

By T.L. Headley, MBA | The Hedley Company

For sixteen years, the 2009 CO₂ endangerment finding was the keystone that held together a regulatory arch bearing down on every coal-fired power plant in America. On February 12, President Trump and EPA Administrator Zeldin knocked that keystone out.

That is not a metaphor. It is an architectural fact. The endangerment finding was the legal predicate for the Clean Power Plan, its successor rules, vehicle greenhouse gas standards, and the ever-present threat of tighter CO₂ limits that made long-term coal investment untenable even when plants were commercially viable. Remove the predicate, and the regulatory structure built upon it loses its legal foundation.

The administration is right to call it the largest deregulatory action in American history. For the coal industry, it is more than that. It is the removal of the existential regulatory threat that has shaped — and distorted — every major utility investment decision for a generation.

The production data this week underscores why this matters operationally, not just symbolically. U.S. coal output rebounded to 9,453 thousand short tons for the week ending February 7 — up 6.4% from the storm-week low — as logistics normalized and utilities rebuilt stocks. West Virginia’s mines returned to form. Wyoming and Pennsylvania strengthened. Prices firmed across every major basin for the first time since autumn. Rail recovery is underway.

Meanwhile, Warrior Met Coal reported record production at its Blue Creek longwall in Alabama — the result of nearly $1 billion in capital committed years before this week’s headlines, by investors who believed the metallurgical coal market would remain viable. They were right. And now the domestic thermal coal fleet has the policy foundation to make the same argument.

But here is the honest counsel this industry needs to hear: removing the keystone does not automatically rebuild the arch.

Coal plants that have already closed will not reopen. Workforces that have been displaced do not reconstitute overnight. Supply chains that have contracted require time and capital to expand. The infrastructure of a fleet that has been systematically shrunk over fifteen years cannot be restored in a political cycle.

What Thursday’s action does — and this is not nothing; it is enormous — is stop the bleeding. It removes the gun pointed at every plant still standing. It eliminates the legal mechanism by which future administrations could mandate further retirements on CO₂ grounds. It restores investment certainty for operators who have been running month-to-month under the shadow of regulatory risk.

The litigation will come. Environmental groups, state attorneys general, and allied advocacy organizations have already announced their intentions. The cases will work through district courts, circuit courts, and eventually the Supreme Court. That process will take years. And during those years, retained plants will operate, supply chains will strengthen, and the industry will have the time it needs to demonstrate its irreplaceable value to the grid.

That is the task now: demonstrate, week by week, winter by winter, that American coal is not a relic of the past but a load-bearing pillar of the present. This week’s grid data makes that case. Winter Storm Fern made it viscerally. The endangerment finding rescission gives the industry the legal breathing room to continue making it.

The keystone is out. Now the real work begins.

About the Author

T.L. Headley, MBA is a West Virginia native with more than 30 years of experience in energy industry communications, policy, and research. The son and grandson of Logan County coal workers, he brings both a personal and professional understanding of the industries that power America. He holds an MBA from West Virginia University in Business Administration and Economics, an MA from Marshall University in Public Relations and Journalism, and twin Bachelor of Arts degrees from Marshall in European History/Politics and International Relations, with a minor in German language and culture.

Headley served as Communications Director for two of the nation’s largest coal industry trade associations — the West Virginia Coal Association (WVCA) and the American Coal Council (ACC). During his tenure at the WVCA, he founded the Friends of Coal social media platform, which now counts more than 300,000 followers nationwide and generates more than 2 million impressions per month. He is currently President and CEO of The Hedley Company, Communications and Research for Energy, and a founder and Vice President of Communications and Research for The Seneca Center for Energy and Critical Minerals, based in Charleston, West Virginia.

Headley is the publisher of America’s Coal News on Substack and the Coal Currents, Gas Currents, Rare Earth News, and Gridwatch weekly newsletters. He is also the author of several books on the nation’s energy industry, available on Amazon.

About The Hedley Company

The Hedley Company, Communications and Research for Energy, is a full-service public relations and research consultancy serving the nation’s energy sector. Based in West Virginia, the firm provides strategic communications, policy research, media relations, digital strategy, and stakeholder engagement services to leading energy industry associations and companies across the United States. Current clients include the West Virginia Coal Association, the American Coal Council, the Washington Coal Council, the Kentucky Coal Association, and others.

About The Seneca Center for Energy and Critical Minerals

The Seneca Center for Energy and Critical Minerals is an independent research and policy organization based in Charleston, West Virginia, dedicated to advancing sound energy and natural resource policy at the state and national levels. The Seneca Center provides rigorous, fact-based research on coal, natural gas, critical minerals, grid reliability, and energy economics — equipping policymakers, industry leaders, and the public with the information needed to make informed decisions about America’s energy future.

COAL CURRENTS is published weekly by The Hedley Company: Communications and Research for Energy. Data sourced from EIA, AAR, AISI, BLS, USACE, and other publicly available sources. For subscriber use only. All analysis represents editorial opinion.

© The Hedley Company. All rights reserved.