A Publication of The Hedley Company: Communications and Research for Energy

Week Ended April 26, 2026 | Published April 27, 2026

Seneca Center for Energy & Critical Mineral Research

EXECUTIVE SUMMARY

The U.S. natural gas market in the week ending April 26, 2026 is running one of the most paradoxical price configurations in recent memory: Henry Hub at its lowest close since October 2024, while U.S. LNG terminals operate at near-record throughput and European and Asian spot prices trade at historic premiums. The mechanism is the Strait of Hormuz crisis, now in its ninth week, which has removed approximately 20% of global LNG supply from seaborne markets while leaving the domestic U.S. supply-demand balance in a spring shoulder-season surplus.

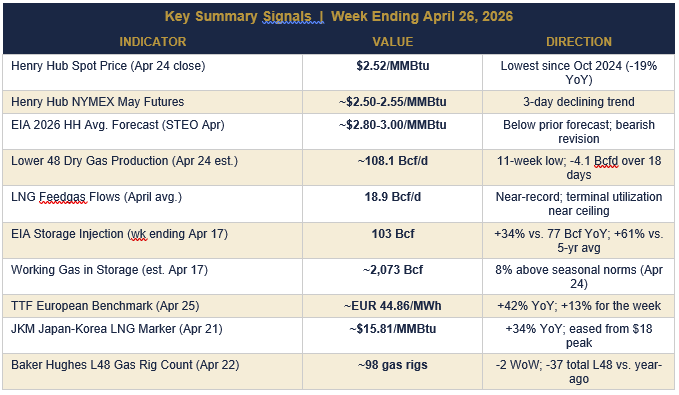

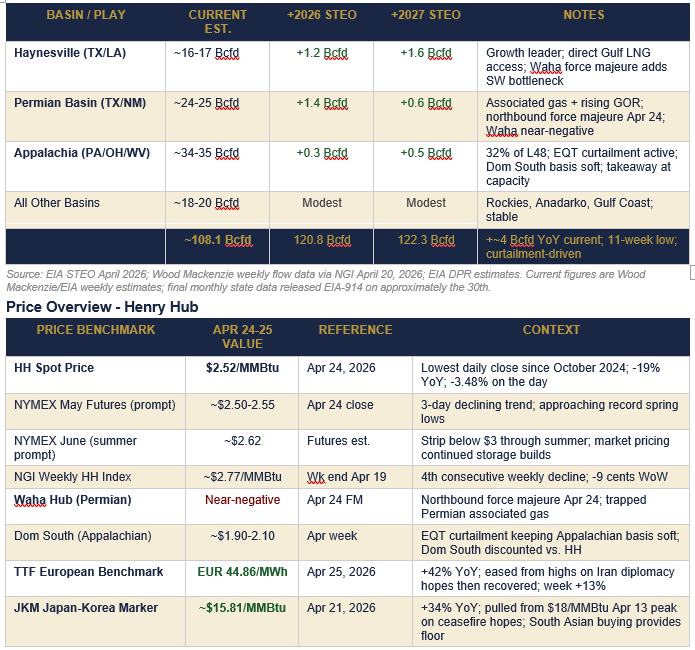

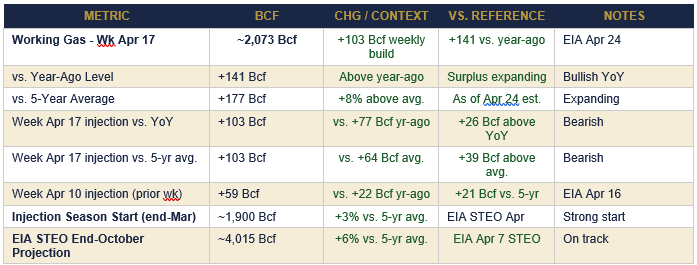

Henry Hub closed at $2.52/MMBtu on Thursday, April 24 - the lowest daily close since October 2024 and approximately 19% below year-ago levels. The 103 Bcf EIA storage injection reported for the week ending April 17 came in well above the 77 Bcf injected the same week in 2025 and 39 Bcf above the 64 Bcf five-year average. Working gas is tracking approximately 8% above seasonal norms. Lower 48 dry gas production slipped to an estimated 108.1 Bcf/d - an 11-week low - as EQT Corporation and other Appalachian producers curtailed output in response to sub-$3.00 pricing. A Permian Basin northbound force majeure on April 24 compounded the bearish domestic price signal, sending Waha Hub prices toward negative territory.

The LNG picture is the structural counterweight. Feedgas flows are averaging 18.9 Bcf/d in April - near the physical ceiling of installed capacity. EIA’s April STEO estimated March LNG exports at 17.9 Bcf/d, the second-highest monthly record. Golden Pass LNG shipped its first cargo. The Trump administration invoked the Defense Production Act for natural gas transmission and LNG capacity as part of a five-memo energy package signed April 20-22, formally classifying gas infrastructure as a national defense industrial resource. Globally, diplomatic efforts to reopen Hormuz collapsed this week as Iranian FM Araghchi’s circuit through Pakistan, Oman, and Moscow produced no agreement and Trump canceled the U.S. delegation’s trip to Islamabad. The TTF-to-Henry Hub spread remains near $10-11/MMBtu net of liquefaction - an extraordinary margin for U.S. LNG exporters.

Overall insight: The central tension this week is between an oversupplied domestic market (storage 8% above norms, HH at 16-month low) and a structurally undersupplied global LNG market (Hormuz closed, TTF +42% YoY). U.S. LNG export terminals are the bridge between these two worlds - and they are running at maximum capacity. The EQT curtailment and Permian force majeure establish a production floor; summer cooling demand is the catalyst for domestic price recovery.

SECTION 1 - U.S. Natural Gas Production & Price Report

Week Ending April 26, 2026 | Sources: EIA STEO April 2026; Wood Mackenzie; EIA-914; NGI

Production Overview

Lower-48 dry gas production is estimated at approximately 108.1 Bcf/d for the week ending April 24 - an 11-week low and a decline of approximately 4.1 Bcf/d over the prior 18 days. Wood Mackenzie data for the week ending April 12 estimated production at 109.9 Bcf/d, still nearly 4 Bcf/d above the same week in 2025. The pullback is driven by voluntary curtailment: EQT Corporation, the Appalachian Basin’s largest producer, explicitly reduced output in response to the sustained sub-$3.00 Henry Hub environment. Canadian net imports fell to approximately 4.9 Bcf/d, down 1.0 Bcf/d from the same week in 2025, further tightening the continental supply picture. EIA’s April STEO projects marketed production at 120.8 Bcf/d in 2026 and a record 122.3 Bcf/d in 2027, with 69% of growth from Haynesville, Permian, and Appalachia - a projection that assumes prices sufficient to support drilling activity.

Market context: The TTF-to-Henry Hub spread of approximately $10-11/MMBtu (net of ~$3-4/MMBtu liquefaction and shipping) represents a historic margin for U.S. LNG exporters. The mechanism is the Hormuz LNG disruption removing ~20% of global seaborne supply since February 28. At $2.52/MMBtu domestically against $13+/MMBtu internationally, every Bcf/d of U.S. LNG export capacity is capturing extraordinary returns.

SECTION 2 - U.S. Natural Gas Storage Report

Week Ending April 17, 2026 | Source: EIA Weekly Natural Gas Storage Report (EIA-912), released April 24, 2026

The upcoming EIA storage report (May 1, 2026, covering week ending April 24) will show the impact of the Permian force majeure and peak spring injection conditions. The April 17 print of 103 Bcf exceeded NGI’s pre-report estimate of 94 Bcf, marking the second consecutive above-average injection. At the current pace, end-October storage is tracking toward 4,100+ Bcf - potentially 8-10% above the five-year average. That is the bearish structural ceiling on Henry Hub prices through the summer season.

SECTION 3 - Rig Count & Employment

Week Ending April 22, 2026 | Source: Baker Hughes North American Rotary Rig Count; BLS CES NAICS 211

Employment in the U.S. Natural Gas Industry

BLS April 2026 (seasonally adjusted, March data): Oil & Gas Extraction (NAICS 211) estimated at approximately 115,000-117,000 employees, maintaining the levels that prevailed through Q1 2026 despite the price pullback. The broader natural gas sector - including upstream extraction, midstream pipeline and storage, processing, LNG export operations, and support services - supports an estimated 1.0-1.5 million direct jobs nationally. Average upstream wages remain elevated at approximately $100,000-$120,000 annually for skilled roles. LNG export operations and AI/data-center-driven power demand are sustaining employment and investment levels that would otherwise retreat at $2.52/MMBtu Henry Hub pricing. Next BLS release covering April 2026 employment: May 8, 2026.

State-level wage estimates (annual, direct + support): Texas ~$15-25B; Pennsylvania ~$4-7B; West Virginia ~$0.8-1.2B; Louisiana ~$4-8B.

SECTION 4 - U.S. Domestic Headlines

Ten Key U.S. Stories: Week of April 27, 2026

1. EIA Reports 103 Bcf Injection for Week Ending April 17 - Triple-Digit Build Sends NYMEX Futures Tumbling

Natural Gas Intelligence (NGI) | April 24, 2026

The EIA’s April 24 Weekly Natural Gas Storage Report showed a 103 Bcf injection for the week ending April 17 - above NGI’s pre-print estimate of 94 Bcf, above the 77 Bcf injected the same week in 2025, and 39 Bcf above the 64 Bcf five-year average. NYMEX futures dropped immediately on the print to their lowest since October 2024.

Why It Matters: Confirms the storage trajectory that has been building all injection season: well above seasonal norms, expanding the year-over-year surplus, and establishing the primary bearish overhang on Henry Hub prices through the spring shoulder season.

2. Henry Hub Closes at $2.52/MMBtu - Lowest Since October 2024 - as EQT Curtails Appalachian Output in Response to Low Prices

Trading Economics / Natural Gas Intelligence | April 24, 2026

Henry Hub closed at $2.52/MMBtu on Thursday, April 24 - down 3.48% on the day, the lowest close since October 2024, and approximately 19% below year-ago levels. EQT Corporation and other Appalachian producers reduced output in response to sub-$3.00 pricing, taking Lower 48 dry gas production to an 11-week low of approximately 108.1 Bcf/d. The four-week NGI index average has declined in four of the last five weeks.

URL: https://tradingeconomics.com/commodity/natural-gas

Why It Matters: The EQT curtailment is the market’s self-correcting mechanism: below-cost pricing triggers voluntary supply reduction, which establishes a production floor and builds the foundation for a recovery when summer cooling demand materializes.

3. Permian Basin Northbound Force Majeure Declared April 24 - Waha Hub Prices Crater Toward Negative Territory

Natural Gas Intelligence / Platts | April 24, 2026

A force majeure was declared restricting Permian Basin northbound pipeline capacity on April 24, trapping associated natural gas in the Permian and sending Waha Hub spot prices toward negative territory. Permian producers face the choice of accepting distressed Waha pricing, rerouting gas south, or curtailing associated production alongside oil output.

URL: https://naturalgasintel.com/data-snapshot/daily/SLAHH/

Why It Matters: The Permian force majeure compounds the Appalachian curtailment: both of the U.S.’s largest gas-producing regions are simultaneously experiencing price-driven production stress. This dual-basin signal reinforces the supply-side floor argument and supports the case for a Henry Hub recovery to $3.00+ when cooling degree days arrive in June.

4. Trump Administration Invokes Defense Production Act for Natural Gas Transmission and LNG Capacity

The Hill | April 22, 2026

One of five DPA determinations in the Trump administration’s April 20-22 energy package covers natural gas transmission infrastructure and LNG export capacity. The Section 303(a)(7) waiver authorizes the Secretary of Energy to make direct purchases, financial commitments, and contract instruments to expand natural gas transmission and LNG capacity. The $1 billion in the 2025 tax and energy law is available through September 30, 2027.

Why It Matters: The DPA determination is the statutory framework that converts the current LNG export boom moment into durable capital infrastructure investment. Pipeline developers, compressor station operators, and LNG terminal owners can now access federal financing for expansion projects that have been stalled by capital access or regulatory timing - at the precise moment the market is demonstrating maximum export economics.

5. Golden Pass LNG Ships Inaugural Cargo - 10th U.S. LNG Export Terminal Now Operational

EIA / ExxonMobil / QatarEnergy | April 2026

Golden Pass LNG (ExxonMobil/QatarEnergy) shipped its first LNG cargo from Sabine Pass, Texas, making it the 10th U.S. LNG export terminal in service. Train 1 will ramp to approximately 1.3 Bcf/d over several months, with full three-train capacity projected at approximately 2.6 Bcf/d. U.S. April feedgas is averaging 18.9 Bcf/d - near the physical ceiling of installed capacity.

URL:

Why It Matters: Golden Pass came online at the most favorable spread environment in U.S. LNG history - the TTF-to-Henry Hub net margin is approximately $10-11/MMBtu. Every additional Bcf/d of U.S. export capacity deployed at this spread level represents a structural demand addition to the domestic gas market and a significant revenue capture for U.S. producers and liquefiers.

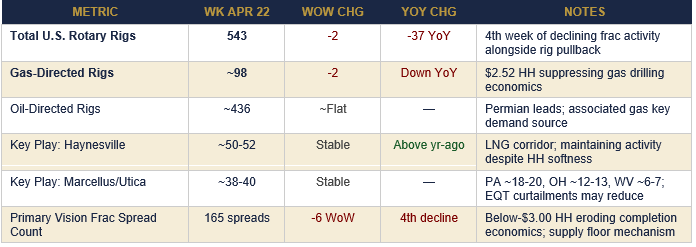

6. Baker Hughes: L48 Rig Count Falls 2 to 543 - Fourth Week of Declining Activity as $2.52 HH Suppresses Drilling Economics

Baker Hughes | April 22, 2026

Baker Hughes reported the Lower 48 rotary rig count fell 2 units to 543 for the week ending April 22 - 37 below year-ago levels. The Primary Vision hydraulic fracturing spread count declined 6 to 165 spreads. Gas-directed rigs are responding to the sustained $2.50-2.80/MMBtu environment. The combined rig and frac count decline is the fourth consecutive week of declining completion activity.

URL:

Why It Matters: The activity pullback is the structural mechanism that will eventually reduce production growth, narrow the storage surplus, and enable a price recovery. Producers maintaining capital discipline at $2.52/MMBtu are the foundation for a tighter supply-demand balance in Q3 and Q4 2026.

7. EIA STEO April 2026: Production Growth to Outpace LNG Exports; End-October Storage at 4,015 Bcf (+6% vs. Avg)

U.S. Energy Information Administration | April 7, 2026

EIA’s April Short-Term Energy Outlook projects marketed production at 120.8 Bcf/d in 2026 and a record 122.3 Bcf/d in 2027. Full-year 2026 LNG exports are forecast at 17.0 Bcf/d, up from 16.4 Bcf/d in the January forecast. End-October storage is projected at approximately 4,015 Bcf - 6% above the five-year average. The EIA states explicitly that production growth will exceed the combined growth in electric power demand and LNG exports, enabling above-average storage builds.

URL: https://www.eia.gov/outlooks/steo/pdf/steo_full.pdf

Why It Matters: The STEO’s production growth thesis - which was set April 7, before the EQT curtailments deepened and the Permian force majeure hit - may now be too bullish on supply. If curtailments persist through Q2, the end-October storage projection could soften, creating a modest price recovery catalyst.

8. DOE Approves 13% Export Authorization Increase for Plaquemines LNG - Adds 0.5 Bcf/d of Non-FTA Market Access

U.S. Department of Energy / EIA STEO April 2026 | March-April 2026

The Department of Energy approved a 13% (0.5 Bcf/d) increase in Plaquemines LNG’s authorization to export to countries without a U.S. free trade agreement, expanding Venture Global’s market access to European and Asian non-FTA buyers. The authorization enables Plaquemines to pursue spot market premiums in TTF-linked European contracts and JKM-linked Asian markets.

URL: https://www.eia.gov/outlooks/steo/pdf/steo_full.pdf

Why It Matters: At current TTF and JKM pricing, non-FTA authorization effectively unlocks the highest-margin spot cargo market available to U.S. LNG exporters. The DOE approval at this moment - when the spread between domestic and international prices is near historical maximums - is both commercially significant and strategically well-timed.

9. Corpus Christi Stage 3 Train 5 Reaches Substantial Completion in March; Exports Set to Begin 2Q26

Cheniere Energy / EIA STEO April 2026 | March-April 2026

Corpus Christi LNG Stage 3 Train 5 reached substantial completion in March 2026 and is set to begin commercial LNG exports in the second quarter of 2026. Each train adds approximately 0.45 Bcf/d of feedgas demand. Combined with Golden Pass Train 1, approximately 0.9 Bcf/d of new nameplate export capacity is coming online in 2Q26.

URL: https://www.eia.gov/outlooks/steo/pdf/steo_full.pdf

Why It Matters: The 2Q26 capacity additions arrive into the widest export margin environment since U.S. LNG exports began. Feedgas is already averaging 18.9 Bcfd and at least one terminal operator is deferring scheduled maintenance to capture the full spread window. These additions push U.S. installed nameplate capacity toward approximately 20 Bcfd by mid-2026.

10. MISO and PJM Reporting Accelerating Data Center Gas-Fired Generation Requests; 2026 Summer Power Burn Growth Expected

EIA STEO April 2026 / Grid Operators | April 2026

ERCOT, PJM, and MISO are all reporting accelerating interconnection requests for gas-fired generation driven by data center loads. EIA’s April STEO forecasts summer 2026 commercial electricity demand growth of 2.6% - driven primarily by data centers - and total electricity demand growth of 1.2% for the full year at 4,108 BkWh. Every additional GW of 24/7 data center capacity running on gas adds approximately 0.15 Bcf/d of incremental power burn.

URL: https://www.eia.gov/outlooks/steo/pdf/steo_full.pdf

Why It Matters: Summer power burn growth is the primary domestic catalyst for Henry Hub price recovery. If data center-driven commercial demand and residential cooling degree days both run above normal in July and August, the storage injection pace could slow materially, moving the end-October trajectory from 4,100 Bcf toward 3,900 Bcf and supporting a Henry Hub recovery to $3.00-$3.50.

SECTION 5 - International Headlines

Ten Key International Stories: Week of April 27, 2026

1. Iran-Hormuz Diplomacy Collapses - Araghchi Tours Pakistan, Oman, Moscow Without Breakthrough; Strait Remains Blocked

Axios / NPR | April 24-27, 2026

Iranian FM Araghchi completed a weekend diplomatic circuit through Pakistan, Oman, and Moscow without producing a Hormuz reopening framework. Iran submitted a new proposal to reopen the Strait while postponing nuclear discussions; Trump canceled the U.S. delegation’s trip to Islamabad. The dual blockade - Iranian shipping attacks and U.S. naval blockade of Iranian ports - remains in force. Iran has removed approximately 20% of global LNG supply from seaborne markets since February 28.

URL: https://www.axios.com/2026/04/27/iran-us-hormuz-strait-nuclear-talks-proposal-pakistan

Why It Matters: Each week of continued Hormuz closure is a week of structural demand for U.S. LNG in European and Asian markets. The diplomatic collapse this week removed the near-term ceasefire risk that had briefly pulled Newcastle below $130/MT and TTF below EUR44/MWh - the LNG supply premium is not resolving in the near term.

2. TTF Falls Toward EUR44/MWh on Iran Ceasefire Hopes, Then Recovers - Still +42% YoY; Week +13%

Trading Economics | April 24-27, 2026

European gas futures fell toward EUR44/MWh on Friday, April 25 on reports of possible U.S.-Iran talks, reversing a four-day winning streak. TTF settled at approximately EUR44.86/MWh before recovering Monday as talks failed to materialize. For the week, European gas prices are up more than 13%. TTF remains +42% year-over-year. EU gas storage is below the trajectory needed for comfortable winter refilling.

URL: https://tradingeconomics.com/commodity/eu-natural-gas

Why It Matters: TTF’s sensitivity to diplomatic signals confirms that the Hormuz risk premium is a real and quantifiable component of European gas prices - not just a headline narrative. The EUR44-45/MWh trading range represents the market’s assessed probability-weighted cost of a supply disruption that has no near-term diplomatic resolution.

3. JKM Japan-Korea LNG Marker Settles in Mid-$15s as South Asian Spot Buying Provides Floor; Japan Inventories Stable

Canada LNG Group / Global LNG Hub | April 13-21, 2026

JKM for the week ending April 17 settled in the low-USD $16s/MMBtu from the high-$16s the prior week. JKM spiked to $18/MMBtu on April 13 when Trump ordered the Hormuz blockade, then retreated on ceasefire expectations. South Asian buyers (India, Bangladesh, South Korea) provided a demand floor in spot markets. METI reported Japan LNG inventories for power generation at 2.20 million tonnes as of April 5, stable week-on-week.

URL: https://www.canadalnggroup.com/natural-gas-prices-weekly-update-jkm-ttf-and-henry-hub-20-april-2026

Why It Matters: The JKM-to-Henry Hub spread at approximately $13/MMBtu sustains maximum U.S. LNG export economics for all terminal operators. South Asian spot buying that is preventing a deeper JKM decline is additional structural support for U.S. cargo demand - these buyers are explicitly replacing Hormuz-disrupted Persian Gulf LNG with U.S. and Australian cargoes.

4. EIA: U.S. LNG Exports Hit 17.9 Bcfd in March - Second-Highest Monthly Record; Full-Year 2026 Forecast Raised to 17.0 Bcfd

U.S. Energy Information Administration | April 7, 2026

EIA’s April STEO estimates March 2026 U.S. LNG exports at 17.9 Bcfd - 8% above the January forecast and the second-highest monthly record after December 2025. The Hormuz disruption widening domestic-to-international price spreads is the explicit driver. The full-year 2026 forecast is raised to 17.0 Bcfd. EIA projects 2027 LNG exports at 18.6 Bcfd. Terminal utilization rates in 2026 are expected to be near maximum capacity.

URL: https://www.eia.gov/outlooks/steo/pdf/steo_full.pdf

Why It Matters: The March LNG export record came before Golden Pass Train 1 and Corpus Christi Stage 3 Train 5 were fully operational. April feedgas at 18.9 Bcfd is already running above the March pace. The trajectory points to a full-year 2026 LNG export outcome that could exceed the EIA’s already-raised 17.0 Bcfd forecast if the Hormuz disruption persists through the year.

5. EU ‘AccelerateEU’ Energy Package Mandates Storage Fills by August 2026 - Structurally Locks In European LNG Demand

European Commission / Reuters | April 23, 2026

The EU’s 16-page AccelerateEU energy crisis package establishes a coordinated framework requiring member states to reach specified gas storage fill levels by August 2026. EU Energy Commissioner Jorgensen projected elevated gas prices ‘for a couple of years’ and acknowledged the EU needs to eliminate gas dependency ‘as fast as possible.’ The package also flagged a potential jet fuel and diesel shortage, with Lufthansa already canceling 20,000 summer flights to save fuel.

Why It Matters: The August 2026 EU storage fill requirement is a regulatory demand anchor for U.S. LNG that is independent of spot price negotiations. Even if Hormuz partially reopens, European buyers must continue purchasing LNG aggressively through the summer injection season to meet the mandatory fill requirement. This is locked-in demand for U.S. Gulf Coast exporters through at least August.

⚑ Carbon Brief flagged per editorial standards. EU Commission source cited directly.

6. Renewable Energy Overtook Coal as World’s Largest Electricity Source in 2025 - Ember Report

Ember via Carbon Brief | April 24, 2026

Thinktank Ember reported that global renewable energy surpassed coal as the world’s largest electricity source in 2025, driven primarily by Chinese solar deployment. The finding is a statistical threshold in aggregate annual generation share. Natural gas’s generation share in the mix is not specifically cited as declining in the Ember data.

Why It Matters: This statistical milestone will be used by investment community advocates to pressure institutional investors to exit fossil fuel holdings. The policy and investment response matters more than the statistic itself. Natural gas’s role as the dispatchable backbone of grid reliability - a role renewables cannot replicate without storage that does not yet exist at scale - is unaffected by the aggregate generation share comparison.

⚑ Carbon Brief flagged per editorial standards.

7. Colombia Hosts First Global Fossil Fuel Transition Summit - 60 Nations; U.S. Not Participating

Carbon Brief / Reuters | April 24-29, 2026

Approximately 60 nations gathered in Santa Marta, Colombia for the First International Conference on the Just Transition Away from Fossil Fuels (April 24-29), following the failure to achieve a formal transition roadmap at COP30 in Brazil in November 2025. The U.S. is not participating. The summit is proceeding in the same week the EU is scrambling to fill gas storage, the U.S. has invoked wartime industrial authority for natural gas infrastructure, and Japan and South Korea are burning more gas than ever.

Why It Matters: The gap between the Santa Marta agenda and the energy security posture of the world’s largest economies has never been wider in a single week’s news cycle. The practical policy lesson of the Hormuz crisis - that fuel security requires diverse, controllable supply rather than weather-dependent intermittent generation - is the strongest argument for natural gas investment running directly counter to what is being discussed in Colombia.

⚑ Carbon Brief flagged per editorial standards.

8. China’s Coal Generation Rose 2% in March Despite Policy Pledges to ‘Strictly Control’ Coal Use

Carbon Brief / Chinese Government Sources | April 24, 2026

China’s coal-fired generation rose approximately 2% in March per CREA analysis, driven by switching from gas to coal amid the Iran War supply disruption. Separately, China released two new policies committing to strictly control coal use and grading local governments on climate targets.

Why It Matters: China’s actual energy behavior - switching to coal when gas supply tightens - is a direct illustration of what happens to any economy when LNG supply is disrupted. The policy declarations are a separate matter from the operational reality. For U.S. LNG exporters, China’s continued gas demand is a structural long-term market regardless of policy rhetoric.

⚑ Carbon Brief flagged per editorial standards.

9. Canada LNG Phase 1 Remains on Track for 2026 Exports - Competing Pacific LNG Source for Asian Buyers

Canada LNG Group | April 2026

LNG Canada Phase 1 (14 Mt/year capacity) remains on schedule for 2026 inaugural exports, adding a new Pacific-facing LNG supply source for Asian buyers. Canadian AECO gas prices have firmed in anticipation of the feedgas demand pull. LNG Canada represents the largest energy infrastructure project in Canadian history.

URL: https://www.canadalnggroup.com/natural-gas-prices-weekly-update-jkm-ttf-and-henry-hub-20-april-2026

Why It Matters: LNG Canada is the primary new competing supply source that could narrow JKM prices for Asian buyers over the medium term. In the current Hormuz crisis environment, LNG Canada�’s Pacific-facing capacity is incremental supply into a severely undersupplied market - it is additive to the demand for global LNG rather than a competitive threat.

10. India Accelerating LNG Regasification Capacity; Long-Term U.S. Supply Agreements Expanding

Petroleum Planning Analysis Cell / Reuters | April 2026

India continues expanding LNG regasification infrastructure and is actively seeking additional long-term supply agreements with U.S. exporters. India’s gas demand growth is structurally driven by industrial and power sector expansion in a country that has historically relied on coal for approximately 75% of its electricity. Indian buyers were among the active spot LNG purchasers in the week ending April 17, per Kpler shipping data.

URL:

Why It Matters: India is the single largest near-term growth market for U.S. LNG. At current JKM pricing, U.S. Gulf Coast cargoes delivered to Indian regasification terminals are competitive with any available alternative. Multi-year supply agreements being finalized now will lock in demand that supports Haynesville and Gulf Coast drilling economics through the 2030s.

SECTION 6 - Legislative, Regulatory & Judicial News

Ten Key Regulatory Developments: Week of April 27, 2026

1. DPA Determination: Natural Gas Transmission and LNG Capacity Classified as National Defense Industrial Resources

White House / The Hill | April 20-22, 2026

Presidential Determination No. 2026-08’s companion determinations covering natural gas transmission infrastructure and LNG export capacity authorize the Secretary of Energy to make direct purchases, financial commitments, and contract instruments under DPA Section 303(a)(7) without standard procurement constraints. The $1 billion in the 2025 tax and energy law is available through September 30, 2027.

Why It Matters: The DPA natural gas determination is the federal authorization framework that enables direct investment in pipeline expansions and LNG terminal capacity additions that market financing alone has not produced fast enough. DOE implementing guidance has not yet been published - watch the Federal Register for a solicitation framework that will define which projects qualify.

2. Federal Register: DPA Energy Package Published April 23 - FR Doc. 2026-08010 and Companion Determinations

Federal Register | April 23, 2026

Presidential Determination No. 2026-08 (coal) and companion determinations covering petroleum, natural gas transmission and LNG, electric grid infrastructure, and large-scale energy development were published in the Federal Register on April 23, 2026 (91 FR 21927). The formal publication starts the clock for DOE implementing guidance on all five determinations.

Why It Matters: The Federal Register publication date is the legal effective date for DOE authorization to begin making purchases and financial commitments. Firms with qualifying projects should begin preparing documentation now - DOE guidance will define the application framework, but the underlying authority is active.

3. EIA STEO April 2026: Full-Year LNG Exports Raised to 17.0 Bcfd; Production to 120.8 Bcfd; Storage End-October 4,015 Bcf

U.S. Energy Information Administration | April 7, 2026

EIA’s April Short-Term Energy Outlook raised the full-year 2026 U.S. LNG export forecast to 17.0 Bcfd (from 16.4 Bcfd in January) and projects marketed production at 120.8 Bcfd. End-October storage is projected at 4,015 Bcf - 6% above the five-year average. The report notes the Hormuz disruption as the driver of above-forecast LNG exports and near-maximum terminal utilization. EIA projects production growth will exceed combined growth in LNG exports and power demand, supporting above-average storage builds.

URL: https://www.eia.gov/outlooks/steo/pdf/steo_full.pdf

Why It Matters: The STEO’s production growth forecast is now the most important variable to watch. If EQT curtailments persist and Permian force majeures recur, the 120.8 Bcfd figure will prove too high - which would be bullish for prices in Q3 and Q4 2026. Monthly EIA-914 data will provide the first definitive evidence.

4. FERC Pipeline Activity: NGA Certificate Reform Prospects Improve as DPA Framework Creates Competing Authorization Pathway

FERC / Industry Sources | April 2026

The DPA natural gas transmission determination implicitly creates a competing federal authorization pathway to the Natural Gas Act Section 7 certificate process for infrastructure projects with a national defense nexus. Legal practitioners are watching whether DOE can use DPA authority to advance projects stalled in FERC’s NGA review - particularly LNG-linked pipeline expansions where eminent domain and environmental review timelines have blocked completion. No formal FERC-DOE coordination guidance has been published.

URL:

Why It Matters: This is the most significant permitting development in the natural gas infrastructure space since FERC’s 2020 certificate policy update. If DOE and FERC coordinate on the DPA-NGA interface, it could unlock a pipeline of Haynesville and Gulf Coast projects that have been in FERC queues for 2-4 years without resolution.

5. DOE Plaquemines LNG Export Authorization Increase: +13% (0.5 Bcfd) to Non-FTA Countries

U.S. Department of Energy / EIA STEO | March-April 2026

The DOE approved a 13% increase in Plaquemines LNG’s export authorization to non-FTA countries, adding approximately 0.5 Bcfd of export capacity to markets without U.S. free trade agreements. This enables Venture Global to sell spot cargoes directly to European and Asian non-FTA buyers at current TTF-linked and JKM-linked premiums.

URL: https://www.eia.gov/outlooks/steo/pdf/steo_full.pdf

Why It Matters: Non-FTA authorization is the commercial linchpin for accessing the highest-margin spot cargo markets. At current spreads, a single Bcf/d of non-FTA authorized LNG export capacity generates approximately $10-11/MMBtu in net margin above domestic procurement costs. The Plaquemines authorization increase is worth hundreds of millions of dollars annually at current pricing.

6. PHMSA LNG Safety Standards NPRM: 60-Day Comment Period Closes Mid-April; Industry Response Filed

PHMSA / Industry Sources | April 2026

The 60-day comment period on PHMSA’s proposed updated LNG facility safety and siting standards closed in mid-April. Industry groups representing LNG terminal operators and peak-shaving utilities filed comments arguing that several proposed seismic and environmental review requirements would extend siting timelines for small-scale LNG facilities used for utility load balancing. PHMSA is expected to publish a final rule in late 2026.

URL: https://www.phmsa.dot.gov/lng-safety-standards-proposed-rulemaking

Why It Matters: Updated LNG safety standards are a routine regulatory matter for large-scale export terminals but could create material constraints for peak-shaving and small-scale LNG infrastructure that supports winter reliability in the Northeast and Midwest. The interaction between PHMSA’s rulemaking and the DPA’s authorization for LNG facility investment is worth watching.

7. EPA Power Plant Rule Reconsideration Advancing - Final Action Expected 2H26 with Gas Dispatch Implications

EPA / Bloomberg Law | April 2026

The EPA’s formal reconsideration review of the Biden administration’s 2024 power plant rule - which required CCS implementation at coal plants and certain gas plants by the 2030s - is advancing toward a final action expected in the second half of 2026. Reversal of the gas plant CCS requirement would remove a regulatory cost overlay on gas generation assets and improve the economics of new combined-cycle gas plant investment.

URL:

Why It Matters: The power plant rule is the most consequential pending EPA action for natural gas demand. If the CCS requirement for new gas plants is withdrawn, new combined-cycle capacity becomes straightforwardly economic in PJM and MISO markets where data center interconnection queues are creating urgent demand. That is a structural long-term demand driver for Haynesville and Permian gas.

8. House Natural Gas Permitting Reform Act Advances; Bipartisan Interest Growing in Wake of Hormuz Crisis

E&E News / Congressional Record | April 2026

The House Natural Gas Permitting Reform Act, which would streamline FERC NGA certificate proceedings and impose timelines on interstate pipeline reviews, is gaining bipartisan interest following the Hormuz crisis demonstration that U.S. LNG export capacity is a national security asset. Multiple Senate offices have signaled support for attaching permitting reform provisions to must-pass legislation.

URL:

Why It Matters: Permitting reform is the single most impactful legislative action for domestic natural gas infrastructure. The Hormuz crisis has created the political environment for a permitting reform bill that has been stalled for years - the argument that LNG exports are a defense and foreign policy tool now has direct, current events evidence behind it.

⚑ E&E News flagged per editorial standards.

9. SEC Climate Disclosure Uncertainty Continues - Court Stays Pending as E&P Companies Navigate Scope 1/2/3 Requirements

SEC / Natural Gas Intelligence | April 2026

SEC climate disclosure rules requiring quantified Scope 1 and 2 emissions reporting and material Scope 3 disclosure for large accelerated filers remain subject to court stays pending appeals. The uncertainty is creating compliance cost planning challenges for publicly traded E&P companies, particularly smaller independents in Appalachia and the Haynesville.

URL:

Why It Matters: SEC climate disclosure uncertainty is the regulatory overhang that most directly affects capital allocation decisions by publicly traded E&P companies. Producers who cannot quantify their future compliance costs cannot provide investors with reliable free cash flow projections - which suppresses both equity valuation and debt access for growth projects.

10. BLM Methane Venting and Flaring Rule Effective for Federal Onshore Leases - Permian Operators Begin Compliance

Bureau of Land Management | April 2026

The Bureau of Land Management’s finalized methane venting and flaring rule is now effective for oil and gas operations on federal onshore leases, setting capture percentages and waste minimization standards. The rule affects approximately 15% of U.S. natural gas production, primarily Permian Basin operators with significant federal lease exposure.

URL: https://www.blm.gov/methane-venting-flaring-final-rule-2026

Why It Matters: The BLM methane rule arrives at a moment when Permian associated gas is already under stress from northbound pipeline force majeures. Capture requirements may accelerate operator decisions to install compression and gathering infrastructure - which could actually support gas takeaway capacity in the Permian and reduce the frequency of Waha Hub negative pricing events.

SECTION 7 - SWOT Analysis

Editorial Mode: Late-April 2026 - A Comprehensive View of Market Dynamics

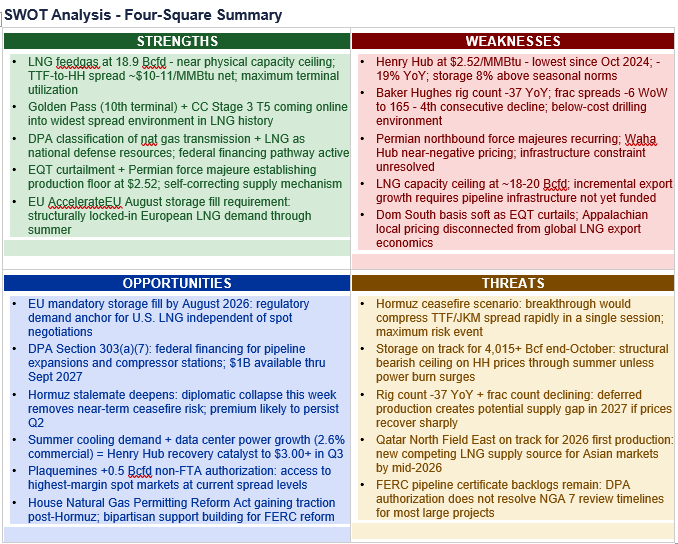

Strengths

The U.S. natural gas sector exhibits its most extraordinary export economics in history. LNG feedgas at 18.9 Bcfd - near the physical ceiling of installed capacity - demonstrates that the Hormuz disruption has created a demand pull that is maxing out current export infrastructure. Golden Pass LNG shipped its inaugural cargo, making it the 10th U.S. terminal in service. The TTF-to-Henry Hub net spread of approximately $10-11/MMBtu represents a margin that has no historical precedent in duration or magnitude. EIA’s April STEO projects full-year 2026 LNG exports at 17.0 Bcfd - up from 16.4 Bcfd in January - and 2027 exports at 18.6 Bcfd. Production at 108-110 Bcfd demonstrates the sector’s structural supply capability even while voluntary curtailments manage the domestic price signal. The DPA determination classifying natural gas transmission and LNG as national defense industrial resources creates a federal financing framework for infrastructure investment that has no precedent in the modern regulatory era. Baker Hughes production curtailment - EQT explicitly reducing Appalachian output - demonstrates producer discipline that establishes a supply floor and builds the foundation for price recovery.

Weaknesses

Henry Hub at $2.52/MMBtu is the lowest closing price since October 2024 and approximately 19% below year-ago levels. Storage is building 8% above seasonal norms - tracking toward an end-October level of 4,015 Bcf or higher - which creates the bearish structural ceiling on domestic prices through the summer shoulder season. The Baker Hughes rig count at 543 is 37 below year-ago levels, and the Primary Vision frac spread count has declined in four consecutive weeks to 165 - confirming that $2.52/MMBtu is below the economic threshold for incremental gas drilling. Permian northbound force majeures are recurring, demonstrating that Waha Hub infrastructure constraints are not resolved and that the Permian associated gas growth story is subject to periodic price dislocations. Dom South Appalachian basis remains soft relative to Henry Hub as EQT curtailments reduce local clearing demand. The LNG capacity ceiling at approximately 18-20 Bcfd means additional export demand growth from Golden Pass Train 2 and subsequent trains requires more pipeline infrastructure before it can be realized.

Opportunities

The EU’s AccelerateEU mandatory storage fill requirement - which must be met by August 2026 - creates structurally locked-in demand for U.S. LNG that is independent of spot price negotiations. European buyers must continue purchasing LNG aggressively through the summer injection season regardless of whether Hormuz partially reopens. The DPA natural gas infrastructure determination enables federal financing for pipeline expansions, compressor station upgrades, and LNG terminal capacity additions that have been stalled by capital access or regulatory timing - with $1 billion available through September 2027 under the same 2025 energy law fund as the coal determination. Corpus Christi Stage 3 Train 5 and Golden Pass Train 1 are ramping simultaneously into the widest spread environment in U.S. LNG history, capturing extraordinary revenue during their commissioning periods. Summer cooling demand - particularly from data center-driven commercial electricity consumption growing at 2.6% per EIA STEO - is the primary domestic catalyst for a Henry Hub recovery to $3.00+ by Q3 2026. The EQT curtailment and Permian force majeure reduce the storage build pace and narrow the bearish overhang that is suppressing near-term prices.

Threats

A Hormuz ceasefire scenario remains the single largest near-term threat to the LNG export economics driving U.S. gas market strength. Any breakthrough in U.S.-Iran negotiations would compress the TTF and JKM spreads rapidly - potentially in a single trading session - removing the $10-11/MMBtu net margin that is sustaining terminal maximum utilization and feedgas near-record levels. The diplomatic collapse this week reduced this risk materially, but negotiations are ongoing and a breakthrough remains possible. The above-normal storage trajectory creates a bearish price ceiling that may prevent a Henry Hub recovery from reaching levels that support robust drilling economics, potentially setting up a tighter supply situation in 2027 than the current forward curve implies. The Baker Hughes rig count 37 below year-ago levels, combined with the frac spread count decline, represents deferred production that could create a supply gap in late 2026 or 2027 if prices recover sharply - increasing price volatility. FERC pipeline certificate backlogs remain unresolved for most large midstream projects, limiting the speed at which Haynesville and Permian production can reach LNG export terminals even with DPA authorization.

SWOT Analysis - Four-Square Summary

Strategic note: The central tension in the late-April 2026 natural gas outlook is between an oversupplied domestic market running at a 16-month price low and a structurally undersupplied global LNG market running at near-record export throughput. The bridge between these two realities is U.S. LNG export infrastructure. The DPA determination, the EU storage mandate, and the Hormuz stalemate are three reinforcing factors that make the current LNG export economics more durable than a single-event premium. Operators, investors, and policymakers should focus on the pipeline infrastructure bottleneck as the binding constraint on capturing the next phase of export growth.

ANALYSIS - The Cheapest and Most Valuable Gas in the World: The April 2026 American Natural Gas Paradox

By T.L. Headley | The Hedley Company

Henry Hub closed at $2.52/MMBtu on Thursday. TTF closed the same week at the equivalent of approximately $13/MMBtu. That $10.50 spread, net of liquefaction and shipping costs, is the most extraordinary sustained margin in the history of U.S. LNG exports. And the United States is running its export terminals at near-maximum physical capacity to capture every molecule of it.

That is the paradox of the American natural gas market in the spring of 2026. Domestically, the picture looks bearish by every conventional metric: a 16-month price low, storage building 8% above seasonal norms, the Baker Hughes rig count 37 below year-ago levels, EQT Corporation curtailing Appalachian production, a Permian force majeure sending Waha Hub prices toward negative territory. Read those data points in isolation and you have a textbook oversupply story.

Read them in context and you have something entirely different. EQT’s curtailment is not a crisis - it is the rational response of a disciplined producer to a price signal that is below the marginal cost of new drilling. The curtailment establishes a production floor and begins the process of tightening the supply-demand balance that will support a price recovery when summer cooling demand materializes. The rig count decline is the market telling producers to stop growing supply faster than demand can absorb it. These are healthy, functional market signals.

The global picture is the structural counterweight. The Strait of Hormuz has been effectively closed to commercial LNG shipping since February 28. That closure has removed approximately 20% of global seaborne LNG supply from the market for nine weeks. Europe is scrambling to fill gas storage under an EU regulatory mandate requiring completion by August. Japan and South Korea are drawing on their LNG inventories at rates that require continuous replenishment. South Asian buyers - India, Bangladesh - are actively purchasing spot cargoes to fill the gap left by Persian Gulf supply. Every one of those buyers is looking at U.S. Gulf Coast LNG terminals as the primary available alternative.

The diplomatic efforts to resolve the Hormuz standoff collapsed this week. Iranian FM Araghchi completed a circuit through Pakistan, Oman, and Moscow without producing a framework. Trump canceled the U.S. delegation’s trip to Islamabad. As of Sunday, Araghchi was in Moscow seeking Russian diplomatic backing while the U.S. naval blockade of Iranian ports entered its third week. This is not a situation that is resolving in days. The risk premium embedded in European and Asian gas prices is not an ephemeral trade - it reflects a structural supply disruption with no near-term diplomatic solution.

The Defense Production Act determination signed April 20 is the policy response that will define this moment’s legacy. By classifying natural gas transmission infrastructure and LNG export capacity as industrial resources essential to national defense, the administration has done something that no previous administration attempted: it has placed the federal government’s wartime industrial authority behind the expansion of U.S. natural gas export infrastructure. The Section 303(a)(7) waiver bypasses standard procurement constraints. The $1 billion in the 2025 energy law is authorized and available. DOE implementing guidance has not yet been published - that is the next milestone.

For the industry, the operational priority is straightforward: capture the spread for as long as it persists. At least one terminal operator is already deferring scheduled maintenance to avoid going offline during the highest-margin period in the sector’s history. Golden Pass Train 1 is ramping. Corpus Christi Stage 3 Train 5 begins exports this quarter. Plaquemines received a non-FTA authorization increase. The physical ceiling on U.S. feedgas - approximately 18-20 Bcfd with current infrastructure - is the binding constraint, not demand.

The strategic challenge is building the next layer of infrastructure before the current spread environment closes. Haynesville has production capacity that cannot reach LNG export terminals because of midstream bottlenecks. Permian associated gas is periodically stranded behind northbound force majeures. The pipeline infrastructure investment that the DPA determination enables is not for the current crisis - it is for the next one, and for the structural decade-long demand growth from European diversification, South Asian energy development, and Northeast Asian LNG dependency.

The Santa Marta fossil fuel transition summit proceeding this week in Colombia, with 60 nations deliberating how to phase out the very fuels that are keeping the lights on in Europe and Japan right now, is the most vivid illustration available of the gap between energy policy aspiration and energy security reality. The European Union’s AccelerateEU package, published three days before the summit opened, is a document about how to fill gas storage fast enough to avoid a winter crisis - not a document about transitioning away from gas. Reality writes its own briefs, and in the spring of 2026, reality is firmly on the side of American natural gas.

By T.L. Headley, MBA,

President

The Hedley Company

ABOUT

About the Author

Terry L. Headley, MBA, MA is a veteran energy communicator, strategist, and researcher with more than 25 years of experience at the intersection of energy policy, industrial economics, and public affairs. A former journalist, he has served as a communications director and senior advisor for major energy and natural gas industry organizations, helping shape national and state-level debates over grid reliability, fuel diversity, and energy security. Headley is widely recognized for developing data-driven messaging strategies that translate complex energy and industrial issues into plain language for policymakers, media, and the public.

About The Hedley Company

The Hedley Company is a strategic communications, research, and advisory firm specializing in energy, industrial policy, and infrastructure issues. The firm provides clients with rigorous analysis, message development, media strategy, and thought leadership focused on grid reliability, fuel diversity, critical minerals, and the economic foundations of American industry.

About The Seneca Center for Energy and Critical Minerals Policy

The Seneca Center for Energy and Critical Minerals Policy is a research and policy organization dedicated to advancing serious, fact-based discussion on America’s energy security, electric grid reliability, and critical minerals supply chains. The Center focuses on the strategic importance of traditional and emerging energy resources in supporting national security, economic stability, and industrial competitiveness.

Contact Information

Terry L. Headley, MBA, MA | President, The Hedley Company

Email: [email protected] | Phone: 681.356.1776

169 Raceview Drive, Ona, WV 25545

Seneca Center for Energy and Critical Minerals Policy

Founding Fellow and Vice President, Communications and Research

GAS CURRENTS is published weekly by The Hedley Company: Communications and Research for Energy.

Data sourced from EIA, Baker Hughes, NGI, Wood Mackenzie, LSEG, IEA, BLS, and other publicly available sources. For subscriber use only.

All analysis represents editorial opinion.

AI assistance used in research/drafting under author’s direction; all judgments author’s own.